Understanding the basics of Transfer pricing, mispricing and other aggressive tax planning measures and concepts

Understanding the basics of Transfer pricing, mispricing and other aggressive tax planning measures and concepts

By Moses Kulaba, Governance and economic analysis centre, Dar es Salaam-Tanzania

In a persistent ambition and search to maximize share vale and returns to their beneficial owners, Multinational companies use various means to gain a tax advantage. Some of these advantages are achieved by legally existing means while others such as Transfer mispricing are purposely designed to circumvent existing provision of the tax law. As Countries grapple to increase their domestic resource mobilization, governments, policy makers and tax authorities will need to learn and adapt new techniques to debunk and disrupt the various tactics and schemes used by these MNCs. Such learning and adoption has to take place at a faster than lightning speed and gusto In less developed and resource rich countries where value and wealth is generated and sourced yet little is paid back in the form of taxes.

Transfer pricing is setting of the price for goods and services sold between controlled (or related) legal entities with an enterprise. For example, if a subsidiary company sells goods to a parent company, the cost of those goods paid by the parent is the transfer price.

Transfer price is not illegal if the goods are sold between related parties at an actual comparable price in the market (arm’s length price). However, if the prices are distorted so as to achieve a tax advantage (by either selling below or above the market price), then transfer mispricing or aggressive transfer pricing is said to have occurred which is an illegality.

Multinationals engage in transfer mis-pricing for purposes of achieving a tax advantage by shifting profits from subsidiaries in high tax jurisdiction to low tax jurisdictions. By doing so multinationals pay less or no taxes at all in countries where they have economic activities (generate income) and should be paying taxes.

Demonstration of Transfer pricing arrangements

Figure 1: Transfer pricing arrangements of a telecommunications company-Source: http://thecastreet.com/introduction-to-transfer-pricing

From the above illustration the Company A located in India will sell goods and services worth 120 rupees to its 100% controlled subsidiary Company C located in a tax haven in Dubai and thereafter the Company C will sell to another Subsidiary B located in the US at a higher or inflated price of 130 rupees. The 30 rupees made in profit will be kept in Dubai where the pay company pays 0% tax.

Exemptions & Reliefs

Generous tax breaks and advantages given to a taxable entity for purposes of achieving a given economic or tax objective such as increasing or facilitating investment. Tanzania extends generous incentives and exemptions to foreign investment corporations. In recent times, there is limited evidence to show that tax exemptions and reliefs are major factors influencing investor’s choice of investment destinations. On the contrary they have been used for tax evasion by circumventing the provisions within the law

Round tripping

A self-explanatory term denoting a trip where a person or thing returns to the place where the journey began.

In illicit financing and tax evasion terms, it refers to a situation where money or income leaves the country through various channels such as inflated invoices, payments, to shell companies overseas (tax haven) etc and returns back to the same country as investment for purposes of benefiting from existing gaps and incentives within the Country’s laws.

False Declaration

A deliberate measure by a liable tax payer or corporation to under disclose or not to disclose at all the accurate taxable income or items or services for purpose of reducing the tax payers tax obligations or evading paying taxes completely. Individuals or corporations use this strategy to hide their taxable liabilities from the tax authorities.

Thin Capitalization

Thin capitalisation measures, where a company finances its operations with a high proportion of loans rather than shares and therefore reduces the business profits of its subsidiary in highly taxed jurisdiction and maximises profits via interests paid on the loan to a bank or financial institution located in a lower tax jurisdiction.

Profit laundering and re-invoicing

These methods also include profit laundering and re-invoicing measures; a process which involves transferring profits from a territory in which they would be taxed to another in which there is either no tax or a lower tax rate or a sale to an agent based in a safe tax haven who subsequently sells on to a final purchaser.

The agent pays part of their mark-up price to the original vendor or to the purchaser, usually to an offshore account located in a secrecy jurisdiction

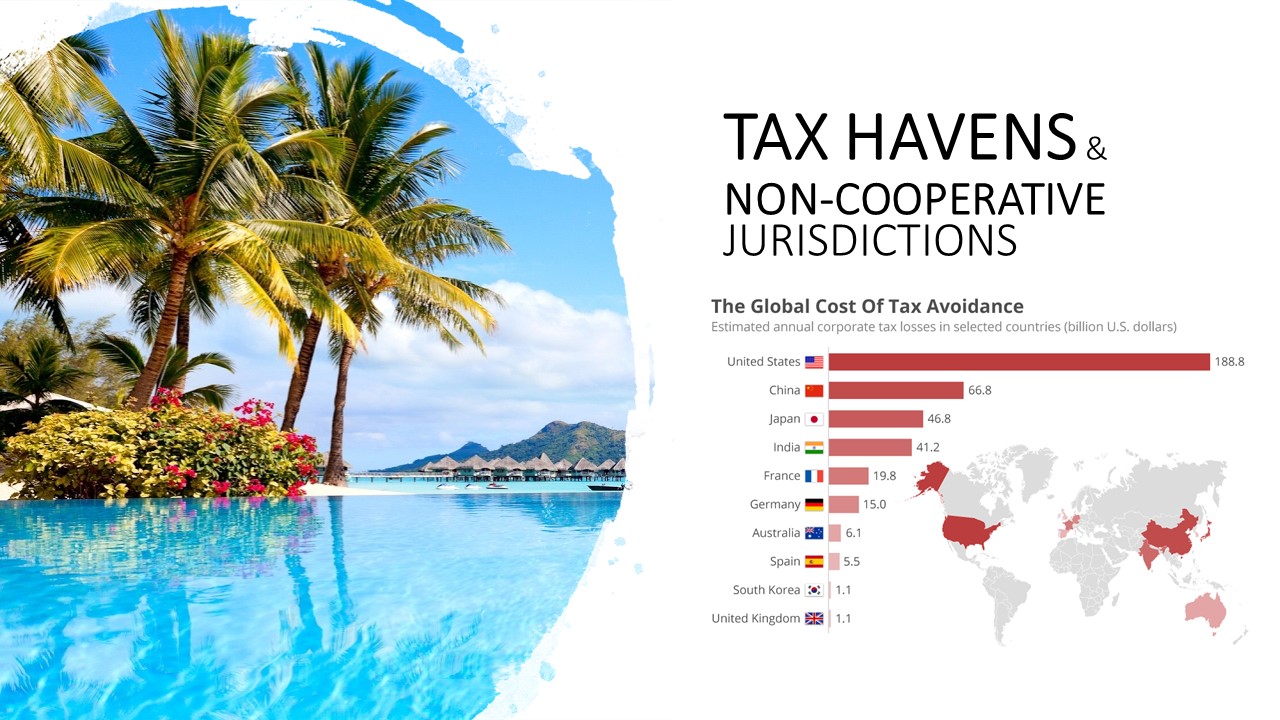

Use of Offshore, Secrecy Jurisdictions and Tax ‘Havens’

The use of low tax jurisdictions or tax havens has become the common strategy for hiding income from the tax authorities.

Tax havens are legal jurisdictions that offer a combination of low tax rates, limited regulations and total secrecy about ownership of registered corporations and individual assets.

In the Cayman Island there is a famous building called Ugland House, a small building, where 12,748 companies are registered and supposedly conduct their business (among them Coca Cola and Intel Corp). However, in reality these are shell companies and postal addresses and no real business activity goes on here. In a sarcastic remark of surprise, the US President Barack Obama on January 5th, 2008 said either this is the largest building in the world or the largest tax scam.

Characteristics of tax havens and examples of ‘Tax Havens’

- Assured Total Secrecy on identity of owners, accounts and operations

- Assured legal assistance

- 0% Corporate tax or Low Tax rates on income

- Financial and Auditing assistance

- Logistics and supplies assistance

- Human Resource Management assistance and facilitation

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected corporations operating in Tanzania and potentially incorporated and using tax havens

|

Extractive Company |

Country (ies) of Incorporation and Subsidiaries |

|

Acacia Mining |

Incorporated in UK. Has 3 subsidiaries in the Cayman Islands, One in Mauritius and one in Barbados |

|

AngloGold Ashanti |

Incorporated in South Africa, Has one subsidiary in the Isle of Man and One in New Jersey |

|

Petra Diamond |

Incorporated in Bermuda |

|

Shanta Gold |

Incorporated in Guernsey |

|

Bezant Resources |

Incorporated in UK. Has one subsidiary in the British Virgin Islands |

|

Orphir Energy |

Incorporated in UK, Has 24 Subsidiaries in Jersey, 14 the British Virgin Islands, 3 in Bermuda and 3 in Delaware |

|

Stratex International |

Incorporated in the UK has 100% owned subsidiaries in Switzerland and 33% owned subsidiary in Jersey |

|

Wentworth Resources |

Incorporated in Canada. Has 3 Subsidiaries in Jersey and in in Mauritius |

|

Statoil |

Incorporated in Norway, with one Subsidiary in Switzerland |

|

Telecommunications |

|

|

Bharti Airtel Tanzania |

Incorporated in India. Has 25 subsidiaries in the Netherlands and one in Jersey |

|

Milicom (Owns Tigo) |

Incorporated in Luxemburg. Has 4 subsidiaries in the Netherlands |

Estimated value of wealth held in Tax Havens

The actual estimates of the total size of wealth held in tax havens is not quite clear. However it is estimated that

- The value of assets held offshore, either tax-free or subject to minimal tax, was estimated in 2015 at over US$11.5 trillion; over one-third of global GDP;

- It is estimated Developing countries lose over $385 billion annually to tax dodging by wealthy individuals, profits laundering by companies and to untaxed activities in the grey economy

- Recent financial leaks show that wealthy Africans hide their wealth in tax havens

- It is estimated that USD 500 billion in financial wealth is kept offshore amounting to 30% of all the financial wealth held by Africans.

- It is estimated that African Countries are among the fastest growing but capital flows to tax havens are one factor limiting the benefits of economic growth for ordinary Africans.

Comparison of living standards of poor families in Tanzania and the Caribbean tax havens

Examples of some documented tax planning cases reported in Tanzania

Examples of cases of Tax planning measure undertaken by companies to benefit from the various exemptions under the Investment Act and Customs and Excise Acts have been reported in Tanzania.

- In the matter of the Commissioner General Vs Geita Gold Mining Ltd which appeared before the Tax Revenue Appeals Tribunal (Originating from Tax Revenue Appeals Board, Case No 22 and 23 of 2004, Geita Gold Mining Limited had failed to pay PAYE as required under section 41 of the Income Tax Act, 1973. In this case a TRA audit revealed that PAYE was paid as additional salary to the employees and recorded as expenses to the company and demanded it to be set off.

TRA argued such an act reduced the taxable income of the respondent and subsequently the tax paid by the company was reduced. Geita had illegally claimed expenses which it was not entitled to.

The Tax Revenue board also made reference to a provision within Geita Gold Mines’ Expatriate Conditions Terms of Service which was aimed at avoiding taxes. Section 3.1 of the expatriate conditions terms of service stated that subject to Article 3.2 the employees offshore Salary component will paid free of local income tax into the employees nominated bank account. All other benefits may attract local taxation. The tax appeals board ruled in favour of TRA.

In 2017 there more reports of tax avoidance and evasion by the Canadian firm Barrick and its local subsidiary Acacia mining companies. The report was tabled by presidential commission appointed to investigate claims and suspicions of tax evasion by the mining firm. Following this report, the government confiscated the company’s consignment of Gold concentrates and required the firm to pay billions of dollars in accumulated tax arrears. The findings from the commission were disputed and negotiations to resolve the dispute were still ongoing

Causes or Aggravating factors for illicit Financial Flows

- Weak legislative framework

- Global Financial Systems which allows capital to move freely across jurisdictions

- Poor –Interagency collaboration

- Limited institutional capacity and technical competency

- Corruption and poor ethical values amongst those entrusted with power and decision making

- lack of Patriotism

Measures or initiatives that are being undertaken nationally and internationally to tackle IFFs

- Establishment and training of international tax departments in National Tax Authorities

- OECD- Base Erosion and Profit Shifting (BEPS) project which seeks to provide guidelines on how multinationals should conduct business abroad and requiring for mandatory disclosure and exchange of information on tax matters.

- Advocacy for wider transparency through initiatives such as Extractive Industries Transparency Initiative (EITI) and Open Government Partnership (OGP).

- Advocacy for governments and companies to publish what they pay and what they earn

- Advocacy for improved reporting of corporate operations such as Country by Country reporting or Project by Project reporting of operations.

Relevant readings

- Marc Curtis, Tundu Lissu: A Golden Opportunity? How can Tanzania is failing to benefit from gold mining; A report for the Christian Council of Tanzania, Tanzania Episcopal Conference and the National Muslim Council of Tanzania, 2015

- Marc Curtis, Dr Prosper Ngowi and Dr Attiya Waris: One Billion Dollar Question: How can Tanzania stop losing so much tax revenue; A report for the Christian Council of Tanzania, Tanzania Episcopal Conference and the National Muslim Council of Tanzania, 2012

- CMI Chr Michelsen Institute: Lifting the veil of secrecy; Perspectives on international taxation and capital flight from Africa, Norway, 2017