How to manage transboundary petroleum resources as Somalia and Kenya talk conflict off East African Coastline

The war of words and negative diplomacy between Kenya and Somalia over the disputed potentially oil and gas rich territory in the Indian Ocean has rekindled the importance of understanding how to manage transboundary petroleum resources. Petroleum does not know political borders. The vagaries of geology have dictated that sometime petroleum resources occur in trans boundary areas. How nation states collectively manage these resources can determine whether they effectively harness the benefits from these resources without going to conflict.

By Moses Kulaba, Governance and economic analysis centre

Management of petroleum resources or revenues from ‘trans boundary or ‘disputed’ areas has always been an issue of controversy in most petroleum resource rich countries. It is a source of disputes and a challenge to investors, planners and policy makers when parties or Countries fail to agree amicably on the ownership of these resources and revenue sharing mechanisms for resources from these areas. Trans-boundary resources are also called ‘common’ or shared resources.

In Tanzania and the wider East Africa region management of resources in ‘potentially contestable areas’ and ‘trans boundary’ areas are becoming a major challenge as some of the petroleum resources are found closer or along the boundary areas. It will be even more challenging in the nearby future as the gas and oil starts flowing. If not addressed it will be a big hindrance to investment and development of the petroleum sector. In East Africa, currently there is no concrete and pragmatic approach to addressing this challenge.

The East African dimension

In a broader East African context, seismic studies have indicated that petroleum resources may be largely found along Trans international boundary areas. This has created disputes and raised challenges for proper resource management and revenue sharing arrangements. For example the discovery of petroleum deposits in the Albertine basin generated trans boundary tensions between Uganda and the DRC along the Lake Albert. There are disputes over petroleum in Unity state along the South Sudan and Sudan border. There are disputes between Kenya and South Sudan along the Nadapal area (Block 11 A & B) and Kenya and Somalia along the Wajir border area (block 1, 2 &3) and Indian Ocean Coastline continental shelf.

In 2014, Somalia filed a before the International Court of Justice, accusing Kenya of encroaching on its potentially rich petroleum rich maritime territory off its continental shelf. Both countries have claimed ownership of an approximately 100,000 square miles in the Indian ocean waters suspected of having vast oil and gas deposits.

The conflict largely arises from a dispute in regards to how the international border between Somalia and Kenya should drawn and internationally recognized. In the case before the ICJ, Somalia wants the maritime boundary to run diagonal, as an extension of the land boundary, while Kenya wants it to run parallel to the latitude, east wards, south of Kyunga. Both countries have relied on the straight-line principle in the International Law of the sea. Somalia wants the boundary to run south east wards and has vowed not surrender what it considers, its territorial integrity.

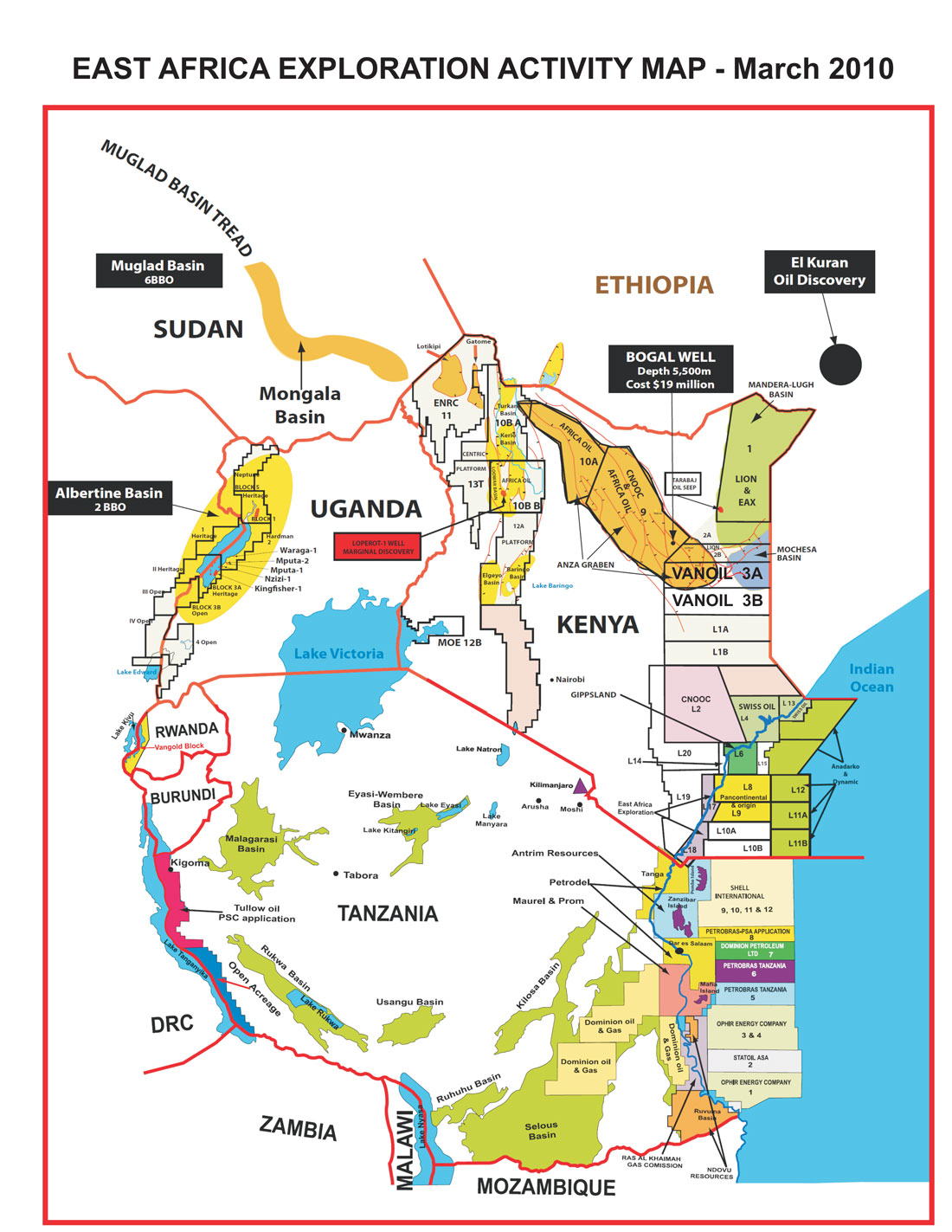

Figure 3: East African Exploration Map 2010-Source: Vanoil Ltd Energy-Kenya

In recent months there has been an escalation the war of words and negative diplomatic relations. Kenya in April barred Somali Officials from entering into Kenya and further banned unaccompanied luggage from Somalia and required that all aircrafts flying into Kenya from Somalia should temporary land in the Northern town of Wajir for a mandatory security check before flying into Nairobi.

The recent diplomatic row represents a significant development between the two neighbors which could escalate into a full-blown out conflict. It further reflects the common resource quagmire that neighboring petroleum rich nation states often find themselves and further shows that latent conflicts emanating from transboundary petroleum resources exist in East Africa.

It is therefore important that viable solutions are reached even without addressing the international law (Law of the sea) challenges facing Kenya and Somalia and the international political concerns or interests in East Africa yet significant challenges and ways of resolving this problem do exist.

Specific problem

- There is lack of clarity for policy makers, planners and tax administrators on how to share the revenues from these areas

- Uncertainty and wavering Investor confidence to fully commit their investment and as a consequence petroleum resources in potentially disputed or Trans boundary areas have remained unexplored. For example, licensed blocks operated by Shell in Tanzania’s waters closer to Zanzibar have remained unexplored for a long time

- On a wider East African level there are missed opportunities for joint investment promotion.

- There is a ‘Race to the bottom’ as East African Countries under cut each other with lucrative fiscal terms in competition to attract petroleum investors into their own territories, without looking at East Africa as a whole

- There are ongoing and underlying territorial disputes which could erupt into full blown out conflicts, risking the current and future investments into the petroleum sector

Currently, a lot has been written about these possible challenges but very limited pragmatic steps have been taken to address these challenges. There has been some significant discussion about the issue but there have been no pragmatic viable options provided which can be acceptable to the protagonists in the conflict.

If some pragmatic solutions are found for Kenya and Somalia, similar suggestions could also be used to inform approaches taken by other East African governments within the wider East African framework to address similar other potential disputes along their border frontiers.

Some international approach to similar challenges

The answer to nature’s conundrum where petroleum resources migrates within or across a country’s border has always been unitization. Unitisation is one of the legal devices which seek to remove the destructive competitive elements stimulated by the rule of capture (as advanced in the United States legal tradition under which the title to petroleum belongs to the owner who physically extracts it from a well on his land, even if petroleum has migrated underground from neighboring lands). With unitisation petroleum deposits are exploited as a whole, expenditure is reduced and recovery is maximized. Unitisation is accomplished through a unitization agreement. A unitization agreement is an amicable solution between parties as individuals, group of individuals or states holding exploitation rights in common petroleum reservoirs by which the reservoirs will be exploited in an integrated manner. The reservoir is treated as one whole and the costs and revenues shared between the parties according to an agreed formula defined by parameters such as geological technical factors, investment or operational costs and volumes of the reservoir. An international unitization agreement (Unit operating Agreement) can be signed between relevant international companies from both states subject to the bilateral treaty outlining the rights and obligations of each company and issues like selection of operator or determination of tract of participants.

International law remedy and Joint Development Areas

The International law remedy to offshore ‘trans international boundary’ petroleum resources is provided within the ambits of the United Nations Law of the Sea Convention of 1982 (UNCLOS) which obliges states which have not been able to agree on boundaries of their continental shelves and exclusive zones to make efforts to enter into provisional arrangements of a practical nature to develop the petroleum deposit located in the overlapping geographical area under dispute whilst not foregoing their sovereignty rights to the deposits in place in its territory or continental shelf.

This international law remedy is the backbone on which the idea of Joint Development Areas or Zones is built. Joint development is an arrangement between two states to develop and share in agreed proportions the petroleum found within a geographical area whose proportions the petroleum found in a geographical area whose sovereignty is disputed; and the geographical area is an overlapping area under dispute with undefined boundaries to which the two states are entitled under International law. The JDA is established by a treaty, agreement or any recognisable legal document stating the rights and obligations of each party. The JDA’s can be divided into separate contract areas where deposits can cross the internal boundaries of those contracts and those that cross the JDA’s into third party states. Both approaches are geared towards securing mutual cooperation and maximizing benefits from the petroleum resources. The treaties or agreements incorporate procedures to minimize disputes and resolve disputes. The following country experiences can be benchmarked:

Possible country experiences for benchmarking

Norway’s experience with United Kingdom

Norway is a good example of the significant economic benefits that can be achieved through strong cooperation and bilateral relationship. Norway has entered various treaties as examples of successful border unitization and management of resources straddling across a vast maritime area between Norway and United Kingdom. On March 10, 1965 Norway and the United Kingdom signed a bilateral delimitation treaty and this agreement constituted the first detailed provisions for action to be taken in the case of a petroleum deposit straddling cross border. This treaty was a voluntary agreement of a maritime border and acceptable cost and revenue sharing formula based on the volume of resources. This treaty provided a basis for three more cross border unitization agreements covering the Frigg, Stratfjord and Murchison Field signed in 1976, 1979 and 1979 respectively.

Norway is also a unique good example of managing Trans boundary petroleum resources by three neighboring states. This experience was demonstrated in the joint management of the Markham Field reserves. In 1965 the United Kingdom and the Netherlands signed a bilateral agreement to establish the boundaries of the Dutch continental shelf, when a petroleum reserve of approximately 700 cubic feet was discovered the licence was awarded to a Dutch company-Ultramar Exploration (Netherlands BV). The discovery was named Markham Field and jointly managed under the Markham agreement signed between the United Kingdom and Norway for unitization of petroleum resources straddling across the maritime borders. The United Kingdom’s health and safety authorities and their Dutch counterparts, the Straatstoezicht op de mijen, had unlimited access to all facilities and information related to the management of the resources. The UK and the Netherlands governments imposed taxes and shared profits as per their fiscal regimes and applicable double taxation conventions The Markham agreement provided a framework for successful development of the field and a possible template for any future unitization between three states

Norway has also taken a pragmatic framework agreement approach in resolving managing Trans boundary petroleum fields without involving distinct intergovernmental treaties. This approach was taken in 2005 by Norway and the United Kingdom in managing the Enoch & Balne Oil fields Norway’s focus has been on securing economic benefits for both states, with provisions made for possible development of resources with infrastructure located on the one side of the boundary. More examples of such approaches include the development of the Boa field which is mostly in Norway and the Playfair fields which are almost entirely in the United Kingdom. Since 2005 Norway has signed more treaties with Russia in the Barents Sea and thus excelled as a champion in managing off shore Trans boundary resources in contentious territories.

East Timor (Timor Leste) and Australia’s experience

In Asia-Timor Leste and Australia are good examples of joint management of Trans boundary petroleum resources. In 2002 East Timor and Australia signed the Timor Sea treaty between the two governments. This treaty enabled the joint development of petroleum resources in the maritime area located between East Timor and Australia. This area also known as the ‘Timor Gap’ had been controversially disputed and subjected to an earlier Timor Gap Treaty in 1989 between East Timor, Australia and Indonesia.

The Timor Sea treaty established a Joint Development Administration (JDA) and provides that Australia and East Timor shall jointly manage, facilitate, exploration, development and exploitation of the resources within the JDA for the benefit of the people of the two countries. The treaty has also provided an acceptable revenue formula whereby 90% of the revenues from the JDA would go to East Timor and 10% would belong to Australia.

The treaty resolved the long political impasse related to the management of the Sunrise and Troubadour petroleum reserves, also collectively referred to as the ‘Greater Sunrise’ which spanned across the Eastern boundaries of the new Joint Petroleum Development Authority (JPDA). The Sunrise and Troubadour deposits were unitized and an acceptable revenue sharing formula agreed. A joint management committee was established to oversee its implementation. To date the approach is a successful model of joint petroleum resource administration in Asia. Similar approaches have been taken by Qatar and United Arab Emirates, Saudi Arabi and Bahrain.

Nigeria and Sao Tome et Principe’s Experience

In cases where countries have longstanding territorial disputes, they can reach out for third parties or independent arbitration panels or international courts of justice to resolve or advice on the best alternative to manage the petroleum resources located in these areas. This approach is referred to as the third-party approach.

This was the approach taken by Nigeria and Sao Tome et Principe in Africa, to create a border upstream cooperation and Joint Development Zones (JDZ) through Unitisation of two major fields (Ikanga and Zafiro) between Nigeria and Equatoria Guinea. On this backdrop, the government of Sao Tome et Principe claimed an archipelago status under Article 46 of the United Nations Conventions of the Law of the Sea (UNCLOS) as based on the 200 miles Exclusive Economic Zone (EEZ) determined by a median line in the North East and the North West as the median line between Sao Tome and Nigeria. The Nigerian government based its claim on the Exclusive Economic Zones Act (CAP 116) and claimed an EZZ which overlapped with Sao Tome et Principe’s zone. The two countries agreed to resolve their differences by creating a Joint Development Zone in the area of overlap to enable exploitation and licensing to proceed. Both countries have since mutual benefited economically.

Relevancy of these Countries’ experience to Tanzania and East Africa’s trans boundary petroleum resources management

As a result of these experiences, unitisation is now a major compulsory feature in petroleum legislations of these countries. The United Kingdom Petroleum Act 1998 and the 1988 Petroleum (Production) (Seaward Areas) Regulations, the Nigerian Petroleum Act of 1969 and the 1969 Petroleum (Drilling and Production) laws impose a compulsory unitization. All licence holders or contractors have an obligatory requirement to agree on a unitization. They are obliged to cooperate if and when reservoirs straddling within or beyond national borders must be developed and it is within the national interests to secure efficient maximum recovery of petroleum. Resources and revenues are managed in agreed manner without losing national or international ownership and sovereignty.

Although the Nigeria and Sao Tome’s case was an arrangement between sovereign states, this approach is relevant to Tanzania, given the similarities of the issues involved. Zanzibar is an archipelago with a specific claim to territorial waters along its coastline. Mainland Tanzania’s 200 miles EEZ overlaps Zanzibar’s territory. Nigeria and Sao Tome’s approach could towards resolving Tanzania’s petroleum resources management challenge with Zanzibar.

These benchmarked examples indicate that geological constrains, territorial disputes, political and economic differences, constitutional limitations and international boundaries should never be a limiting factor to development of petroleum resources located or straddling from one territory to another. Tanzania and the wider East African region can draw alternative solutions to the current challenges facing management of trans boundary petroleum resources:

Possible alternative or supplementing solutions

- In Tanzania, within the current constitutional framework there could be a ‘Partial delegation’ of legal powers to Zanzibar to enter into agreements with oil companies (state and non-state actors) subject to the Union Constitution and the Union government’s Petroleum and fiscal management legislations

- Delimitation of temporary boundaries for oil and gas management purposes and earmarking specific petroleum blocks which could be legally assigned to Zanzibar’s control for revenue purposes

- Establish Joint Development Area (JDA) or Joint Development Zone (JDZ) arrangements modeled successful arrangements like Norway and United Kingdom, Timor Leste and Australia. Agree on unitization arrangements for licensed blocks straddling outside the JDA and develop a revenue sharing formula for managing resources from JDA and Trans boundary areas. Establish a joint petroleum revenue management committee for trans international boundary areas

- Develop East African guidelines for unitization and Joint Development Area Management and revenue sharing for Trans boundary petroleum resources.

- Either off the above approaches could be adapted in resolving the dispute between Kenya and Somalia

Benefits from these options

If resolved this could lead to peaceful co-existence and increased joint attraction of foreign investment into the areas

Increase investor confidence in East Africa and open up new avenues for investment and value creation in its Petroleum sector.

Unfreeze the current blocks which are closer to Zanzibar for licensing, exploration and development. These blocks have remained unlicensed for many years, despite expression of interests from petroleum companies to develop them

Provide avenues for possible cross border petroleum resources development and sharing of petroleum energy resources at low costs and thus reduce the acute shortages of electricity and over reliance on hydroelectricity for power generation in the region.

References

- Beyene, Zewdineh and Wadley, Ian L.G. Common goods and the common good: Transboundary natural resources, principled cooperation, and the Nile Basin Initiative. Berkerley, UC Berkeley: Center for African studies 2004.(Breslauer Symposium on Natural Resources Issues in Africa😉 at pg4

- Cameron P.D: Cross Border Unitisation in the North Sea (Vol. 5 OGEL 2007)

- Denis V.Rodin: Offshore transboundary petroleum deposits: Cooperation as a customary obligation; Small Masters of Laws thesis in the Laws of the Sea; University of Tromso, Faculty of Law, Fall 2011

- Perry A: Oil and Gas deposits at international boundaries-New ways for governments and oil and gas companies to handle an increasingly urgent problem (Vol. 5 OGEL 2007); M.O Igiehon, Present International law on delimitation of the Continental shelf (Sweet & Maxwell 2006

- Rod Chooramum; Notes to the Field: An English law perspective on the oil and Gas Market, August , 2014

- Sustainable Development or Resource Cursed: Managing Timor Leste’s Petroleum Revenue, Chapter 4

- URT: The National Natural Gas Policy, 2013

- Zanzibar Oil, Gas win cools political heat; The East African Newspaper; http://www.lawteacher.net/free-law-essays/australian-law/joint-petroleum-developmet-area.php

- http://www.theeastafrican.co.ke/news/Zanzibar-oil-gas-win-cools-political-heat/-/2558/2877248/-/view/printversion/-/1485oatz/-/index.html. Also read: Oil and gas: How EA Can become a key global player; http://www.theeastafrican.co.ke/oil-and-gas…

- http://www.forbes.com/sites/christopherhelman/2014/01/08/the-10-biggest-oil-and-gas-discoveries-of-2013/ accessed on 19th May 2015 at 7:45 pm