Enhancing the Viability of NDCs in East Africa: Assessing Progress, Gaps and path to net zero

Author: Nader Khalifa, Researcher, Governance and Economic Policy Centre*, December 2025

Introduction: COP30 as the Implementation Milestone

The COP30 in Belém – Brazil marked a critical milestone, being framed as the “Implementation COP,” arriving a decade after the signing of the Paris Agreement and returning to Brazil over 30 years since the landmark 1992 Earth Summit. The COP concluded with some proclamations on Just Transition Mechanism and adoption of Global Goal on Adaptation (GGA) indicators, and increased focus on nature and finance but little radical actions to tame the climate crisis under 1.5°C target.

Despite the milestones, global implementation remains off-track, with countries collectively failing to reduce emissions and scale resilience at the pace required. The climate crisis is still treated with suspicion, geopolitical jostling and underfunded, highlighting a clear gap between ambition and action. Only small share around 12–15% of European climate finance is accessible to the poorest and most climate-vulnerable African countries, far below their share of climate risk and need (OECD, 2023). In East Arica, analysis of climate adaptation finance shows that approximately 52.7 % of funds committed for adaptation were actually disbursed between 2009 and 2018 (Savvidou et al., 2021).

This paper assesses the state of global progress on Nationally Determined Contributions (NDCs), with a particular focus on East African countries—Kenya, Uganda, Tanzania, and Rwanda. It further compares the level of NDC implementation and financial support needs in these countries against the climate finance commitments and disbursements of selected European nations, evaluating whether NDCs remain viable tools for achieving the Paris Agreement objectives, identifying gaps, and proposes strategic recommendations to strengthen their viability in achieving Paris Agreement goals.

Global NDC Assessment: Are We on Track for Paris Targets?

According to the UNFCCC’s latest NDC Synthesis Report (2023–2024), global emissions remain far above Paris-aligned trajectories. Current NDCs collectively put the world on a 2.4–2.6°C warming path far from the 1.5°C target (UNEP, 2023).

NDC Implementation Gap: Structural Barriers and Evidence of Underperformance

Although East African countries have strengthened their Nationally Determined Contributions (NDCs) since 2015—many increasing mitigations ambition by over 20–30% and expanding adaptation priorities—the region continues to face a widening implementation gap as real-world emission reductions have not followed at the required scale. This gap reflects both systemic constraints and insufficient translation of political commitments into measurable action and raises serious questions about whether NDCs, as currently designed, can deliver the Paris outcomes.

Key Implementation Gaps and Challenges

High dependence on external climate finance

- Most East African NDCs rely on 70–90% external financing, particularly for adaptation and energy transition.

- The region collectively requires more than USD 280–300 billion by 2030, yet receives less than 12%–15% of that annually (AfDB, 2023).

- Adaptation finance alone is underfunded by over USD 2.5 billion per year across the region (GCA, 2023).

Limited progress in translating NDC commitments into sectoral action

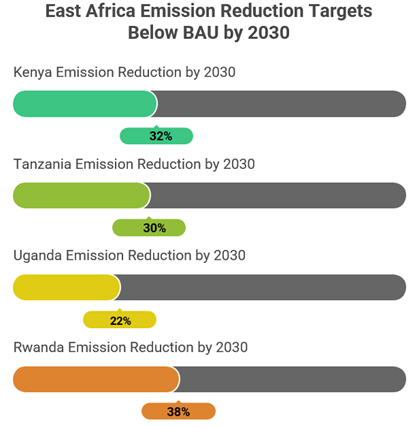

- Updated NDCs include ambitious mitigation targets—such as Kenya’s 32% by 2030, Uganda’s 22%, and Ethiopia’s conditional 68%—yet emissions continue to rise in transport, agriculture, and industry.

- Only 20–30% of planned mitigation actions are currently being implemented at scale.

Weak MRV systems and institutional capacity

- More than 70% of East African countries lack fully operational MRV systems across energy, agriculture, and waste sectors.

- Inadequate data collection and reporting reduce accountability and hinder access to climate finance, which increasingly requires robust tracking frameworks (ICAT, 2022).

Limited domestic integration and mainstreaming

- NDCs remain insufficiently embedded in national and subnational development plans.

- Fewer than 40% of sector ministries align annual budgets with NDC priorities, creating fragmentation and slow execution.

- Local governments—key for adaptation delivery—receive less than 10% of the required climate financing.

Slow and complex climate finance disbursement

- Global climate funds (e.g., GCF, GEF) take 18–24 months on average from concept to approval.

- East Africa adaptation finance disbursement ratio (≈52.7 %), considerably below what’s needed and indicating a persistent delivery gap.

- Private-sector investment remains below USD 4 billion per year, far short of the USD 24–30 billion needed annually.

Limited community participation in planning and delivery

- NDC implementation often excludes rural and climate-vulnerable communities, despite these groups experiencing more than 70% of climate impacts (floods, droughts, crop failures).

- This reduces local ownership and increases the risk of maladaptation.

East African NDCs: Ambition, Progress, and Implementation Realities

The second generation of Nationally Determined Contributions (NDCs) in East Africa demonstrates a clear increase in ambition compared to 2015 submissions. However, implementation continues to lag far behind targets due to systemic financing, institutional, and capacity constraints. This section synthesizes the ambition levels, progress indicators, and the underlying structural barriers limiting effective delivery of NDC commitments in Kenya, Tanzania, Uganda, and Rwanda.

Ambition Levels and Emission Reduction Targets

All four East African countries have strengthened their 2030 climate commitments, reflecting enhanced sectoral coverage (Kenya: Energy, agriculture, LULUCF, transport, waste, Tanzania: Energy, transport, forestry, waste, Uganda: Energy, forestry, agriculture, Rwanda: Energy, industry, waste, agriculture) and improved quantification of mitigation and adaptation actions.

These targets indicate rising ambition; however, nearly 80–90% of planned mitigation outcomes remain dependent on external finance, highlighting an imbalance between national ambition and the available resource base.

- Implementation Status: Progress and Performance

Despite strong stated ambition, real implementation remains uneven and significantly below required trajectories. Key observations include:

Positive Developments

- Kenya continues to lead the region in renewable energy deployment, with geothermal providing over 40% of total power generation, complemented by utility-scale wind and solar.

- Rwanda operates one of the most advanced MRV systems in Africa, integrating national inventories, sectoral reporting templates, and verification frameworks.

- Tanzania and Uganda have made notable progress in adaptation planning, particularly in agriculture, water, and disaster risk management.

However, progress falls short of NDC trajectories due to:

- Delayed and unpredictable international climate finance disbursement, especially for adaptation.

- Limited mainstreaming of NDCs, with weak integration into national development plans, sectoral strategies, and district-level programs.

- Technical gaps in MRV, GHG accounting, emissions modeling, and data management.

- Insufficient private sector participation due to regulatory uncertainty, weak incentives, and few bankable climate projects.

Overall, implementation progress remains slow, fragmented, and insufficient to place the region on a Paris-aligned trajectory.

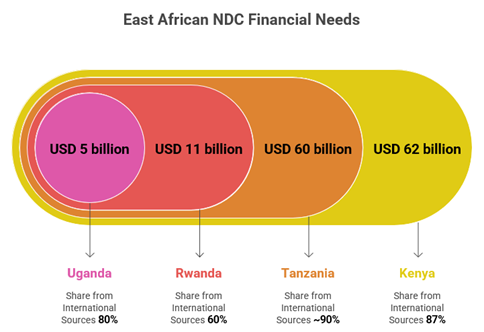

Climate Finance Needs, Delivery, and the Widening Gap

East African NDCs require substantial financing for both mitigation and adaptation. Country estimates highlight an urgent mismatch between required and delivered resources:

Evidence of the Finance Gap

- East Africa receives less than 12% of Africa’s total climate finance inflows (CPI, 2024).

- Adaptation finance remains below 30% of total flows to the region, despite East Africa being among the world’s most climate-vulnerable regions (Brookings Institution, 2022).

- GCF projects in East Africa face approval timelines averaging 24–36 months, slowing implementation of urgent projects.

- National institutions struggle to meet stringent fiduciary and documentation requirements of major climate funds.

Institutional, Governance, and Capacity Constraints

Several deep-rooted challenges hinder NDC implementation:

Institutional Challenges

- Weak MRV systems in several countries limit tracking, reporting, and verification of progress.

- Fragmented inter-ministerial coordination, especially between energy, finance, agriculture, and environment ministries.

- Data deficits in key sectors (LULUCF, agriculture, off-grid energy, transport), affecting GHG inventory accuracy.

Governance and Operational Gaps

- Limited local government engagement, despite significant adaptation actions being subnational.

- Low public participation, particularly in rural and climate-vulnerable communities.

- Few mature, bankable projects, leading to under-utilization of available finance windows.

- Private sector climate investment remains below 15% of total climate finance in East Africa.

Collectively, these challenges reinforce the structural implementation gap, limiting the region’s ability to translate Paris ambition into real, measurable outcomes.

International Climate Finance Support: European Commitments vs. Delivery

-

- Pledges vs. Delivered Finance

European countries — led by Germany, France, the EU, and the UK — collectively pledge significant climate finance to Africa. However, the delivery gap remains substantial:

- OECD data show that while European donors reported USD 34–36 billion in climate finance annually (2019–2022), the actual disbursements to African LDCs were less than USD 9–11 billion.

- Only around 12–15% of European climate finance is accessible to the poorest and most climate-vulnerable African countries.

- Adaptation finance remains critically low: in 2022, EU institutions allocated only 27% of their climate finance to adaptation—far below the 50% target encouraged by COP26 and COP27 decisions.

- The UNFCCC Standing Committee on Finance confirms a USD 1.2–1.3 trillion cumulative finance gaps for African NDCs by 2030.

- According to a report by FSD Africa, the average disbursement ratio for climate finance in Africa is 79%, which includes both mitigation and adaptation flows CPI (2022).

- According to Stockholm Environment Institute (SEI) data, adaptation finance for African countries was disbursed at an average rate of 46%, compared to 56% for mitigation finance.

- The Landscape of Climate Finance in Africa (2024) report from the Climate Policy Initiative (CPI) estimates that adaptation finance flows to Africa rose from USD 11.8 billion in 2019/20 to USD 13.8 billion in 2021/22.

Misalignment with African Priorities

European finance is still mitigation-heavy, although Africa’s most urgent needs relate to adaptation:

- More than 65–70% of EU climate finance to Africa goes to mitigation sectors (renewables, energy efficiency).

- Adaptation sectors such as agriculture, water management, early warning systems, and climate-resilient infrastructure receive less than 30%.

- UNEP’s Adaptation Gap Report indicates that adaptation finance globally is also constrained, Analyses show that a large majority of adaptation actions identified in African NDCs remain unfunded or underfunded, with only around 20–23% of adaptation needs being met by climate finance flows, leaving substantial gaps for implementation. (UNEP Adaptation Gap Report 2023).

- The African Development Bank estimates that Africa needs USD 52–57 billion/year in adaptation finance but currently receives less than USD 11.4 billion/year.

- Systemic Barriers Limiting Access to European & Multilateral Funds

African LDCs face structural constraints that prevent them from accessing European climate finance effectively:

- Approval cycles for GCF and GEF projects routinely takes time, delaying implementation.

- High fiduciary standards, financial reporting requirements, and bankability tests result in rejection or delays for NDC-aligned proposals.

- Only 14 African national institutions are currently accredited to the GCF, limiting direct access.

- Less than 5% of readiness funding reaches local MRV institutions, leading to persistent data gaps.

- Technical assistance for NDC implementation—planning, monitoring, tracking, and verification—remains insufficient for most countries.

This combination makes African NDCs remain “ambitious on paper, underfunded in practice.”

Why NDCs Still Matter

Despite finance and implementation challenges, NDCs remain central to Africa’s climate and development future because they:

- Define and update national climate ambition every five years;

- Guide investment pathways in mitigation and adaptation;

- Anchor national development plans to climate-resilient trajectories;

- Serve as the main framework for accessing climate finance;

- Provide structure for reporting under the Enhanced Transparency Framework.

Strengthening NDC design, financing, MRV, and implementation support is fundamental post-COP30, where countries are expected to raise ambition and demonstrate credible progress.

Policy Recommendations

To close the growing implementation gap and ensure that East African NDCs deliver measurable climate outcomes, the following evidence-based policy actions are proposed. These recommendations strengthen institutional capacity, enhance climate finance access, accelerate sectoral mainstreaming, and improve accountability post-COP30.

- Strengthen Institutional and Technical Capacity

- Establish Dedicated NDC Implementation Units

Create permanent, inter-ministerial NDC coordination units mandated to align sectoral policies, oversee progress, and engage with development partners.

- Upgrade MRV Systems and Technical Competencies

Invest in end-to-end MRV systems—GHG inventories, mitigation tracking, adaptation metrics, and digital monitoring tools—while providing continuous training for sector ministries.

- Develop National Climate Data Repositories

Build centralized climate data platforms for agriculture, energy, transport, and land use to enhance evidence-based policymaking and transparency.

- Enhance Climate Finance Mobilization and Access

- Formulate National Climate Finance Strategies:

Align domestic priorities with the eligibility criteria of the GCF, GEF, Adaptation Fund, and bilateral donors to improve approval rates and reduce project rejection.

- Increase Readiness and Project Preparation Funding

Expand participation in GCF Readiness, NDC Partnership support, and GEF capacity-building programs to address limited pipeline of bankable projects.

- Promote Blended Finance and Private Sector Mobilization

Introduce policy incentives for green bonds, guarantees, concessional loans, and PPPs to unlock long-term mitigation and adaptation investments.

- Advocate for Simplified Access Windows for LDCs

The future COPs must negotiate streamlined procedures, reduced documentation requirements, and faster approval timelines for LDC and fragile countries.

- Mainstream NDCs into National and Local Development Planning

- Integrate NDC Targets into National Budgets and Sector Plans

Embed climate actions in annual budget cycles, Medium-Term Expenditure Frameworks, and district/county development plans.

- Establish Performance Indicators for Line Ministries

Link ministerial scorecards and KPIs with measurable NDC outcomes to strengthen accountability and accelerate implementation.

- Embed Adaptation into Core Sectors

Ensure NDC-aligned adaptation actions are systematically integrated into agriculture, water, health, infrastructure, and urban planning frameworks.

- Scale Up Community and Citizen Participation

- Adopt Community-Based Adaptation (CBA) Frameworks

Expand participatory adaptation programs in rural and climate-vulnerable regions, supported by local extension systems.

- Link Rural Development Programs to NDC Outcomes

Prioritize climate-smart agriculture, reforestation, watershed management, and off-grid energy in rural development interventions.

- Strengthen Gender and Youth Inclusion

Mandate gender-responsive planning and youth representation in NDC committees, local climate governance, and project implementation.

- Enhance Regional Cooperation and Knowledge Exchange

- Establish a Regional MRV and Knowledge Platform

Under the East African Community (EAC), create a shared platform for data exchange, methodologies, and best practices on GHG inventories and sectoral MRV.

- Promote Cross-Border Renewable Energy Corridors

Accelerate regional geothermal, hydro, and solar initiatives, along with power-pool integration and transmission infrastructure.

- Strengthen Transboundary Ecosystem Management

Improve joint management of critical basins—Lake Victoria, the Nile, and rangeland ecosystems—to enhance resilience and disaster risk reduction.

- Improve Transparency, Governance, and Accountability

- Publish Annual NDC Implementation Reports

Introduce open-access dashboards that track emissions, adaptation progress, climate finance flows, and project delivery.

- Create Independent Oversight Mechanisms

Establish multi-stakeholder oversight bodies involving civil society, academia, and the private sector to review progress and recommend corrective actions.

- Mandate Public Disclosure of Climate Finance

Require transparent reporting of all international and domestic climate finance flows, including donor commitments, disbursements, and utilization.

About the Author: Nader Khalifa is an engineer and energy professional with over 15 years of expertise in the energy and petroleum sectors. He currently serves with the Ministry of Energy & Petroleum of Sudan, in addition to his role as a Sudan Team Member for the Initiative on Climate Action Transparency (ICAT) project, a collaborative effort involving UNEP, CCC, and HCENR, and a distinguished researcher and a Colosseum Member at the Governance & Economic Policy Centre (GEPC).

References

- African Development Bank (AfDB) (2023). Climate finance in Africa: Overview and outlook. Abidjan: African Development Bank Group.

- Brookings Institution (2022). Finance for climate adaptation in Africa: Still insufficient and losing ground. Brookings Global Economy and Development Program. Available at: https://www.brookings.edu/articles/finance-for-climate-adaptation-in-africa-still-insufficient-and-losing-ground/.

- Climate Policy Initiative (CPI) (2024). Landscape of climate finance in Africa. London: Climate Policy Initiative. Available at: https://www.climatepolicyinitiative.org/publication/landscape-of-climate-finance-in-africa-2024/.

- FSD Africa & Climate Policy Initiative (CPI) (2022). Landscape of climate finance in Africa. Nairobi: FSD Africa. Available at: https://fsdafrica.org/wp-content/uploads/2022/09/1.-Landscape-of-Climate-Finance-in-Africa-l-Full-report.pdf

- Global Center on Adaptation (GCA) (2023). Africa’s adaptation gap: Climate finance needs and priorities. Rotterdam: Global Center on Adaptation. Available at: https://gca.org/reports/state-and-trends-in-adaptation/.

- Government of Kenya (2020). Updated Nationally Determined Contribution. Nairobi: Ministry of Environment and Forestry.

- Government of Rwanda (2020). Updated NDC Submission. Kigali: Ministry of Environment.

- Government of Tanzania (2021). Updated Nationally Determined Contribution. Dodoma: Vice President’s Office.

- Government of Uganda (2022). Second Nationally Determined Contribution. Kampala: Ministry of Water and Environment.

- ICAT (2022). Guidance for Transparency Frameworks in LDCs. Copenhagen: Initiative on Climate Action Transparency.

- IPCC (2022). AR6 Working Group III: Mitigation of climate change. Geneva: Intergovernmental Panel on Climate Change. Available at: https://www.ipcc.ch/report/ar6/wg3/.

- Nature (2025). Reframing climate finance for Africa. Available at: https://www.nature.com/articles/d44148-025-00353-5

- OECD (2023). Climate finance provided and mobilised by developed countries in 2013–2021. Paris: Organisation for Economic Co-operation and Development. Available at: https://www.oecd.org/environment/climate-finance-provided-and-mobilised-by-developed-countries.htm.

- Savvidou, G., Atteridge, A., Omari-Motsumi, K. and Trisos, C. (2021). Quantifying international public finance for climate change adaptation in Africa. Stockholm: Stockholm Environment Institute. Available at: https://www.sei.org/publications/climate-finance-adaptation-africa/.

- Stockholm Environment Institute (SEI) (2024). How effective is climate finance in assisting farmers in low- and middle-income countries adapt to climate change? Available at: https://www.sei.org/features/how-effective-is-climate-finance-in-assisting-farmers-in-low-and-middle-income-countries-adapt-to-climate-change/

- UNEP (2023). Adaptation Gap Report 2023: Underfinanced, underprepared. Nairobi: United Nations Environment Programme. Available at: https://www.unep.org/resources/adaptation-gap-report-2023

- UNFCCC (2023). Nationally Determined Contributions synthesis report. Bonn: United Nations Framework Convention on Climate Change. Available at: https://unfccc.int/ndc-synthesis-report-2023

Figure 1: Map of forest loss in Tanzania during 2010–2017 and location of ground survey points

Figure 1: Map of forest loss in Tanzania during 2010–2017 and location of ground survey points