Oil and Energy Transition: Why Sudan conflict provides new hope for EACOP

The Sudan conflict is a catastrophe that must be stopped but its unintended consequences provide new optimism for the East African Crude Oil Pipeline (EACOP).

By Moses Kulaba, Governance and Economic Policy Center

With the constant fighting and insecurity along the pipeline and its pumping stations, the South Sudanese government is now open to exploring new opportunities via EACOP to guarantee its future oil exports.

On March 16th the government of Sudan admitted that it cannot guarantee the smooth export of oil from South Sudan, as a year of war has made it difficult to maintain or even protect the pipeline to Port Sudan.

In a letter to major oil companies involved in the oil production and export, Sudan’s Minister of Energy and Petroleum Dr Mohieldin Nam Mohamed Said admitted that the war had made it difficult to provide any guarantees for safety.

He acknowledged that the conflict was hampering the flow of oil to Port Sudan, as it took time to repair pipelines ruptured during the fighting. In addition, there was a telecommunications breakdown between the pumping stations (PS4) and PS5 in Sudan, which were shut down in the midst of heavy fighting. The area was an active military zone and access for repairs was not guaranteed.

As a response the South Sudanese government had declared a force majeure, making production and export impossible and thereby revamping suggestions to explore new possible safer routes for South Sudan’s oil.

The war in Sudan added to the challenges South Sudan faces in maximizing its only major resource – oil – to fund a financially constrained government and other operations. As a consequence of the war, South Sudan’s oil production fell from 160,000 barrels per day in 2022 to 140,000 barrels per day in 2023. This is was more than half of the previous peak of 350,000 barrels per day before civil war broke out in 2013.

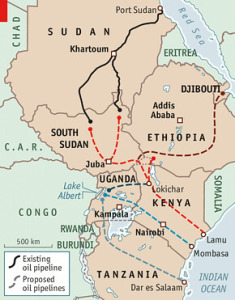

Talks to have South Sudan pump its oil south wards had all along been explored and presented as part of Uganda’s grand plan to make the EACOP an East African project by connecting and supplying all the EAC member states with oil and gas.

Under this grand plan and initial drawings, the Oil pipeline would radiate from its nerve center in Hoima with an artery of pipelines running northwards to South Sudan, westwards to the Democratic Republic of Congo (DRC), eastwards to connect Kenya’s oil from Turkana and southwards with an arm extended to Rwanda and long route via Tanzania to Tanga port.

But the progress of this was partly hampered by Uganda’s fall out with the Kenyan route and the existing agreements signed between Khartoum and Juba during the independence talks. Provisions in these required among others a concession that Sudan will retain territorial control of some oil rich territories and that South Sudan would continue exporting its oil via Port Sudan. By doing this, the government in Khartoum would maintain some revenues from the oil sector that had been largely lost with South Sudan’s cessation and independence.

I remember in a private conversation with a friend from Sudan some years ago he confided that during one meeting with Sudanese youth and young professionals, President Omar Bashir, before his overthrow, had admitted that he was not sure about the economic future of Sudan without South Sudan. He clearly predicted a catastrophic economic meltdown leading to chaos and that was why Sudan had to maintain a grip on South Sudan. The oil pipeline was a win-win infrastructure politically and economically anchoring the two countries as good neighbors.

By Sudan admitting that the safety cannot be guaranteed and reconstruction of the damaged infrastructure will take longer than usual provides South Sudan with a legitimate cause to start exploring new safe routes for its oil.

An oil route from Juba southward would be beneficial to South Sudan, the EACOP but also good for the East African Community as a region. South Sudan derives 90% of its revenues from oil exports and would like to have a constant flow of this oil to sustain its economy. EACOP would guarantee that flow. South Sudan would also have access to other EACOP related infrastructure such as the refinery and international airport for other logistical needs.

An extended pipeline from Hoima northwards to connect with the oil from South Sudan would increase volumes of oil pumped out of EACOP by at least 150,000 to 200,000 barrels per day, increasing EACOP’s profitability and attractiveness to investors.

Moreover, with its oil, South Sudan would become a major regional player with a stronger voice in EAC matters perhaps more than it is today. The pipeline would bring Sudan in the north closer to the EAC, increasing its prospects for joining the EAC and thus facilitating the region’s expansion ambitions.

There could be some differences in the chemical composition and technical aspects of the two oils (Uganda and South Sudan) with perhaps one being waxier than the other but these complexities can be handled through technical re-engineering and design of the oil pipeline.

The EACOP has always been a controversial project with environmental activists and anti-oil crusaders campaigning against its construction. Environmentalists argued that the world’s longest heated pipeline will have serious environmental impacts and contribute to global warming. The future profitability of the pipeline was also questioned given the global push towards a transition away from fossil-based system and uncertainty about the future of oil as an energy source.

None the less, plans for construction of the pipeline are ongoing. Land compensations in Uganda and Tanzania was completed. An advance consignment of pipes was delivered and a coating and insulating plant for the pipelines was commissioned and already operational in Tanzania, paving way for the pipeline construction and ground laying to commence before end of 2024.

The conflict in Sudan therefore provides more impetus to the project as it opens a new door for possible access and increased volumes from South Sudan’s oil and taping into already existing markets can be guaranteed.

The future of oil as a dominant fuel in the global energy system is a controversial subject and a debate exists whether it makes sense to construct new oil pipelines and infrastructure.

However, the crisis and the significance of oil in driving South Sudan’s economy comes at a time when there are all indications that major global super powers such as the United States and United Kingdom are backtracking on their commitments to end and move away from fossil or oil as source of energy.

Despite the announcements made at the COP27 and 28, in his maiden speech to Parliament, King Charles in November 2023 announced that the UK government will issue new licensing rounds for exploration and drilling of oil and gas in the North Sea. The rounds will go ahead each year so long as the UK remains a net importer of oil and gas and if emissions from UK-based production remain lower than those associated with imports.

In the US, Republicans have maintained a firm support for oil and Donald Trump, the most preferred Republican nominee for President has vowed to overturn any existing legislation and commitments made by the Democrats against the fossil energy sector, by signing an executive order to issue new rounds oil and gas drilling. According to Trump this would be his first executive order immediately signed, if he was elected to power in November of 2024. Clearly, the US political will is divided and the future US policy terrain on oil and gas cannot be guaranteed.

Quietly, the leading oil producers are strongly supporting continued pumping of oil. Despite global campaigns, large oil producers are still skeptical that renewables can replace oil in the medium term and by 2050. They believe that the focus should be on decarbonizing oil and not ending its supply and use all together. Ending use of oil would be returning the world to stone age error, one Middle East leader remarked at COP28 before backtracking after coming under intense criticism. The approved language at COP28 was phase down and not phaseout. Oil therefore may have a longer lifetime than earlier anticipated.

Despite the catastrophe that the war has caused, that we all condemn, Uganda and Tanzania should exploit the opportunity it provides to ramp up and conclude talks with South Sudan on the viability of exporting its oil via EACOP.

A study by Ahmed et al in 2017 suggested that Tanzania has an annual technical solar power potential in Tanzania was estimated to be 31,482 TWh for CSP technology and 38,804 TWh for PV technology. Potential solar energy resources are found in the central parts of the country

A study by Ahmed et al in 2017 suggested that Tanzania has an annual technical solar power potential in Tanzania was estimated to be 31,482 TWh for CSP technology and 38,804 TWh for PV technology. Potential solar energy resources are found in the central parts of the country Tanzania has areas of high onshore wind potential that cover more than 10% of its land

Tanzania has areas of high onshore wind potential that cover more than 10% of its land

mate Change Conference, more commonly referred to as Conference of Parties (COP), was held from 6 -18 November 2022 in Sharm El Sheikh, Egypt. This year’s COP was branded as the African COP since it happened on the African continent.

mate Change Conference, more commonly referred to as Conference of Parties (COP), was held from 6 -18 November 2022 in Sharm El Sheikh, Egypt. This year’s COP was branded as the African COP since it happened on the African continent.