The Petals of Blood: Dissecting the contagion effect of Sudan war on South Sudan and EAC with lessons on governance and state failure

The Sudan war has been raging for almost a year, with catastrophic effects now spreading beyond Sudan’s borders, affecting its neighboring South Sudan and the East Africa Community (EAC) in many ways.

By Moses Kulaba, Governance and Economic Policy Centre & James Boboya, Institute of Social Policy and Research (ISCPR), South Sudan

According to the United Nations, since it started, the war has now destabilized the entire region, leading to the deaths of more than 5,000 Sudanese and displacing millions both within the African nation and across seven national borders.[1] Sudan is now home to the highest number of internally displaced anywhere in the world, with at least 7.1 million uprooted.[2] More than 6 million Sudanese are suffering from famine, and these numbers are growing every day. The health system has broken down, and more than 1,200 children have died from malnutrition and lack of essential care. [3]The UN now describes the Sudan conflict as a forgotten humanitarian disaster, while the International Crisis Group has warned that Sudan’s future, and much else, is at stake.

Lest we forget, within a short period, the third largest nation in Africa, with a size of more than 1.8886 million square kilometers and at least 46 million people, has no properly functioning government, and all state institutions have collapsed with the effects of its meltdown spilling over to its neighbors, particularly South Sudan.

South Sudan is host to thousands of Sudanese refugees forced across the border into South Sudan, exerting social and economic pressure on an already fragile state that was already sinking under the burden of its own civil war and internal conflicts.

The Norwegian Refugee Council (NRC) reports that more than 500,000 people have now fled from the war in Sudan to South Sudan. [1]This means that over 30 percent of all the refugees, asylum seekers, and ethnic South Sudanese were forced to flee Sudan since the war exploded in April 2023 for protection in one of the poorest places on earth. “South Sudan, that has itself recently come out of decades of war, was facing a dire humanitarian situation before the war in Sudan erupted. It already had nine million people in need of humanitarian aid, and almost 60 per cent of the population facing high levels of food insecurity.

As of 28 January 2024, more than 528,000 ethnic South Sudanese, Sudanese refugees, and other third-country nationals had crossed at entry points along the South Sudan border into Abyei Administrative Area, Upper Nile, Unity, Northern, and Western Bahr El Ghazal. The majority, 81 percent, entered at Jodrah before making their way to the transit center in Renk. Ethnic South Sudanese who have crossed the border from Sudan are commonly referred to as “returnees.” Still, in reality, many of them were born in Sudan and have never been in South Sudan, and therefore have no kinship connection in host communities.

The conflict has spilled deeper into other East African countries, with thousands seeking refuge and safety from it. The education system collapsed, sending thousands of learners back home and hundreds who could afford to flee exile to continue their studies. Some of these were admitted to Rwandan and Tanzanian Universities.

The Sudan and South Sudan experiment was a governance disaster in the waiting and perhaps serves as a lesson of how a firm grip on power, corruption, and misgovernance can ultimately lead to catastrophic state failure and collapse.

Donald Kasongi, Executive Director of Governance Links and a former senior officer with the Accord, a regional conflict organization, describes the post-Garang South Sudan and post-Bashir Sudan as a protracted governance failure. The diverse strategic roles of Khartoum, Beijing, and Washington in the Sweet South Sudanese oil are now evident. So far, none is a victor.

The role of external interests in shaping national discourse has been at play. Sudan is caught between the interests of the West and the Middle East and China, with both interested in controlling access to Sudan’s resources, cultural wealth, and strategic positioning as a buffer between the North and South. Before the war, Sudan identified itself with the Islamic world and pronounced itself as an Islamic state. Despite this alignment, the OIC and the larger Islamic world has not come to its help. Sudan remains an isolated state left to collapse at its fate.

In South Sudan, the Garang vision of a strong independent nation was lost. After his demise most of the post Garang political elites or military war generals became pre-occupied on restoring the lost years at war by amassing wealth through corruption and sharing out of the limited resources from the oil resources. As a consequence, a strong nation is yet to be built. They had won the war but lost their country. The same mistake plays out in Sudan. Perhaps the conflict is a lesson on what it means to lose what is so dear to one- A country.

In short, the transition in both countries (Sudan and South Sudan) were not well managed and what we see are petals of blood from toxic flowers of bad governance which have flourished like a forest planted along the banks of the river Nile.

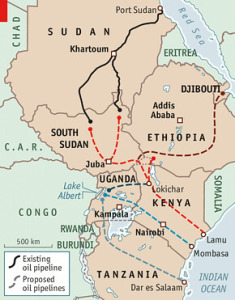

According to James Boboya, the Executive Director of the South worrisome. The raging war has made South Sudan’s oil exports via Port Sudan difficult. Oil exports have collapsed by more than half from 160,000 barrels per day in 2022 to 140,000 barrels per day in 2023. This was more than half of the previous peak of 350,000 barrels per day before civil war broke out in 2013.[2] The South Sudanese dollar collapsed in value. There is a financial crunch and the South Sudanese government has not paid its public and civil servants for months. There is a risk of insurrection and demonstrations by public servants that will be likely joined by the military. This would plunge South Sudan into chaos and total collapse just like its Northern neighbor.

Moreover, this conflict and its associated effects comes in an election year for South Sudan. The general elections are viewed as a watershed moment which may see a transition from President Salva Keir to a new cadre of leadership. With the economic crunch, South Sudan may not be able to organize and fund a credible general election. This will be not good for South Sudan’s democracy and desired future.

With the world’s media focused on the Russia-Ukraine war and the Israel-Gaza wars, little is covered about the Sudan conflicts nor the total economic catastrophe that South Sudan faces.

If not addressed, the Sudan war will be soon inside the borders of the EAC. Can the EAC afford to stand by and watch longer as its member state, collapses. Mediation efforts led by Kenya and Djbouti were postponed last year. Direct talks between Abdel Fattah al-Burhan, Sudan’s army chief and de facto head of state, and General Mohamed Hamdan Dagalo, known as Hemedti, head of the RSF paramilitaries remain futile. What can South Sudan and the EAC do now to avert further catastrophe?

During a joint webinar organized by the Governance and Economic Policy Center (GEPC) and the Institute of Social Policy and Research (ISCR) in South Sudan in April, a distinguished panel of experts discussed and enabled us to understand the contradictions and magnitude of this war with implications and lessons on extractive governance, and state collapse drawn for East Africa and Africa generally, can be taken to avert the situation and its contagion effect on the EAC and Africa generally. The panelists and participants highlighted some key lessons and takeaways that can be drawn from the conflict.

Key lessons and takeaways

Ethnicization of politics and governance can lead to a spiral of violence and catastrophic state collapse, especially when the strong ruling elite and regime finally lose control of power.

A previously united Sudan started getting balkanized when the ruling elites started practicing the politics of ethnicity and religion pitting the largely Muslims in the northern and western parts of the country against their Christian southerners. The Christians were portrayed as slightly inferior, denied political and economic opportunity, and subjected to forced Islamisation, and inhumane conditions such as slavery. Faced with what was considered unbecoming conditions the Southerners opted for a rebellion and demand for independence. The first and second Sudanese civil war (including the Sudanese Peoples Liberation Movement (SPLM/A) were born and the political dynamics in Sudan changed for decades after. New factions such as the Sudanese Liberation Army (SLA) and the Justice Equality Movement (JEM) emerged and Sudan never remained the same. Sentiments for cessation and independence in Darfur flared and faced with an insurgency, President Omar enlisted militias including the Janjaweed to quell the rebellions. Around 10,000 were killed and over 2.5 million displaced. The balkanisation of Sudan was continuing to play out.

Militarisation of politics erodes democratic values and principles which can take decades to rebuild.

Omar Bashir came to power in 1989 when, as a brigadier general in the Sudanese Army, he led a group of officers in a military coup that ousted the democratically elected government of Prime Minister Sadiq al-Mahdi after it began negotiations with rebels in the south. Omar Bashir subsequently replaced President Ahmed al-Mirghani as head of state and ruled with the military closely fused into the politics and governance of Sudan.

The military elites elevated to power during President Omar Bashir’s government enjoyed privileged positions. Even with his overthrow in 2019, these generals maintained a firm grip on the Transition Military Council and the Civil-Military Sovereignty Council. These are less likely to accept any position below total control of the central authority. The net effect is that the return to full civilian and democratic rule of state governance in an entrenched militarized political environment such as Sudan can or may take decades to be rebuilt.

Vulnerability to geopolitical manipulation and fiddle diddle can be a driver to political instability and eventual weak governance

Both Sudan and South Sudan have been victims of well-orchestrated geopolitical game plans from external powers interested in taking control of the rich natural resources wealth that these countries possess. Sudan and South Sudan have vast oil deposits and forestry products. With eyes focused on these resources external powers succeeded in playing one community against another and one country against the other and successfully throwing the region into an abyss of endless crisis. Religion was used as a tool to play the North against the South and continues to be used in some segments of the Sudanese and South Sudanese communities.

Key Takeaways

- The East African Community (EAC) governments cannot afford to take a wait-and-see attitude. The problems facing Sudan and South Sudan are latently present in several other EAC countries. For this reason, therefore without taking lessons from Sudan and South Sudan other countries can also easily erupt in the future, bringing down the entire EAC. The EAC has therefore an obligation to ramp up support for the resumption of the peace process and finding lasting solutions for peace and tranquility in the two countries. For this to happen there has to be trust and objectivity of the actors to the crisis and the EAC mediators.

- Stop ethnicization and militarization of politics and state governance: The Sudan experience demonstrates this, whereby the collapse of President Omar Bashir’s strong grip on power let loose the lid off a can of worms that had eaten the state to its collapse. Similar conditions of ethnic rivalry in state governance have created uncertainty about guaranteed stability in South Sudan. In some other EAC member states there have been attempts to elevate dominant ethnic groups to power and military influence in state politics built around one strong leader. The Sudan experience demonstrates that the absence of such a strong leader holding the center together can lead to a lacuna, leading to a trail of conflict and instability leading governance to fall apart and eventual state collapse.

- The EAC countries must stop viewing at South Sudan as merely a market but as an independent viable state whose stability is good for the entire region. According to the EAC trade statistics, South Sudan was the leading market for goods from Uganda and Kenya. With a total population of 11 million and a collapsed agricultural and industrial base, South Sudan has provided a ready market for agricultural goods and manufactured goods from Uganda and Kenya. According to UN Comtrade Data Uganda exported goods worth USD483.9Mln and Kenya’s exports to South Sudan were worth USD170Mln. Uganda’s exports to Sudan also increased by 154% from around USD48Mln in 2016 to USD123Mln in 2022. With the eyes largely focused on trade opportunities, there can be a tendency to lose track of the human suffering that the people in these countries face. Also, the jostle for geopolitical control over trade deals can overwhelm the genuine solidarity intentions of good neighbors. The EAC members should focus on the stability of these countries.

- The International Community Must not give up on Sudan and South Sudan. Despite the donor fatigue and reports of corruption, the international community has a moral obligation to continue engaging with the protagonists in the war, facilitating the avenues for a peaceful resolution of the conflict and providing humanitarian aid to the suffering people. The Sudan and South Sudan conflict must be treated with equal measure with the Ukraine-Russia, Israel, and Gaza conflicts. The EAC must scale up diplomatic efforts and be an Anchor in Chief in this process, coordinating and connecting Sudan, South Sudan to the world.

- The EAC media and Civil society must continue highlighting the suffering in Sudan and South Sudan. With the Israel and Gaza war ongoing, the Sudan and South Sudan stories that were largely covered by the Western media have since died out. There has been little coverage given within the EAC of the recent developments in this war and how it is affecting its neighbors. Moreover, with limited internet connectivity and restrictive conditions, communication advocacy from inside Sudan and South Sudan is quite difficult. The media and civil society in the EAC therefore must speak loud on behalf of their Sudanese counterparts

[1] War in Sudan displaces over 500,000 to South Sudanhttps://www.nrc.no/news/2024/january/sudan-refugees-to-south-sudan/#:~:text=%E2%80%9CMore%20than%20500%2C000%20people%20have,the%20poorest%20places%20on%20earth.

[2] The East African Business Khartoum unable to ensure smooth export of South Sudan oil https://www.theeastafrican.co.ke/tea/business/khartoum-unable-to-ensure-smooth-export-of-south-sudanese-oil-4564064

[1] Sudan conflict: ‘Our lives have become a piece of hell’ https://www.bbc.com/news/world-africa-67438018

[2] War in Sudan: more than 7 million displaced – UNhttps://www.africanews.com/2023/12/22/war-in-sudan-more-than-7-million-displaced-un//

[3] More than 1,200 children have died in the past 5 months in conflict-wrecked Sudan, the UN sayshttps://apnews.com/article/sudan-conflict-military-rsf-children-measles-malnutrition-ec7bb2a1f49d74e7b5f01afa12f16d99