Tragedy of Conflict, Economic Exclusion, and Meeting Public Economic Expectations in Times of Crisis: The Case of South Sudan

Authors: Boboya James Edimond, Institute of Social Policy Research, South Sudan & Moses Kulaba, Governance and Economic Policy Centre

South Sudan continues to face profound economic and governance challenges rooted in prolonged conflict, institutional fragility, and structural economic exclusion. Despite abundant natural resources, particularly oil, the country has struggled to convert this wealth into broad-based economic development and improved social welfare. Persistent instability, weak public institutions, and economic mismanagement have exacerbated poverty and constrained the state’s capacity to meet public expectations for economic opportunity and effective service delivery.

This paper examines the interplay between conflict, economic exclusion, and public expectations during periods of crisis in South Sudan. Drawing on recent economic assessments and development literature, it argues that sustainable recovery requires comprehensive institutional reforms, economic diversification, and inclusive governance capable of addressing structural inequalities and restoring public trust.

Furthermore, the analysis contributes to ongoing regional debates on East African Community (EAC) national budget plans and the broader implications of the US–Israel–Iran war on energy and economic outlooks in the region. The conflict involving the United States, Israel, and Iran has caused major disruptions in global energy markets, including sharp rises in oil prices and risks to key chokepoints such as the Strait of Hormuz, which carries roughly 20% of the world’s oil supply (2026 Strait of Hormuz crisis). These external shocks underscore the need for prudent, timely resource allocation and resilient fiscal frameworks to support post‑conflict reconstruction and strengthen regional economic resilience.

- Introduction

South Sudan gained independence in 2011 amid widespread optimism about the prospects for peace, political stability, and economic transformation. However, the country soon experienced severe political instability and violent conflicts that undermined its development trajectory. The outbreak of civil war in 2013 and recurring localized conflicts since then have significantly weakened the economy, damaged infrastructure, and displaced millions of citizens.

Conflict has had devastating effects on economic activity, reducing agricultural production, disrupting trade networks, and discouraging private investment. As a result, economic growth has remained fragile and heavily dependent on oil revenues. The country’s economic structure is highly vulnerable to external shocks, particularly fluctuations in global oil prices and disruptions to export infrastructure.

Recent economic assessments indicate that South Sudan’s economy has experienced sustained decline over several consecutive years. The economy was projected to contract by approximately 30 % in the 2024/25 fiscal year, largely due to disruptions in oil production and declining export revenues (World Bank, 2025). Resources mobilized or provided by development partners for post-conflict reconstruction have often been misused, while the country’s narrow tax base further constrains domestic revenue generation. In addition, annual national budgets have frequently been delayed or left unpassed before the National Assembly, undermining fiscal planning and disrupting efforts toward post-conflict reconstruction and development.

At the same time, citizens continue to expect the government to deliver economic stability, employment opportunities, and improved public services. This growing mismatch between public expectations and state capacity has emerged as one of the defining governance challenges in South Sudan, exacerbating public dissatisfaction and weakening trust in state institutions.

Contribution to the Ongoing Debate: EAC Budgets and the Implications of the US, Isreal and Iran War.

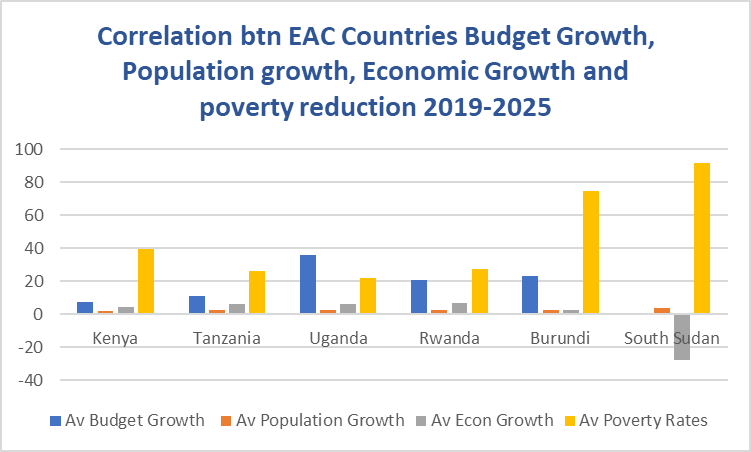

The analysis presented in this paper also contributes to broader discussions in regional dialogues, such as webinars and policy forums, on the East African Community (EAC) national budget plans and the implications of the US-Israel-Iran war for the region’s energy and economic outlooks. The EAC’s collective capacity to plan and implement effective national budgets is increasingly strained by both internal fiscal weaknesses and external shocks. As of the 2023–24 fiscal year, multiple EAC member states — including South Sudan — have experienced significant budget shortfalls and delayed remittances to the regional budget, impeding the bloc’s ability to fund operations and coordinate shared developmental priorities (EAC Secretariat, 2025).

The recent Middle East conflict between the United States and Iran — especially disruptions around the Strait of Hormuz — has major implications for global energy markets and regional economic stability. Roughly 20% of the world’s oil and natural gas trade flows through this strait, so prolonged tensions have driven up global oil prices and heightened supply chain risks, with ripple effects across Africa, including East Africa (Arita, S., Chakravorty, R., Kim, J., Lwin, W. Y., & Steinbach, S., 2026).

For EAC economies that are net importers of energy, the surge in crude oil prices increases the cost of fuel, transportation, and basic commodities, complicating fiscal planning and national budget implementation. Analysts have already warned that East African countries may face rising inflationary pressures, depreciating currencies, and widened current account deficits as a result of these disruptions. This trend makes it more difficult for governments to allocate resources toward development priorities while managing macroeconomic stability.

These regional debates underscore the interconnectedness of domestic fiscal policies and global geopolitical dynamics. They highlight the importance of strengthening EAC fiscal frameworks and diversifying energy sources to mitigate the economic fallout from international conflicts — a theme that aligns closely with the findings of this study on South Sudan’s economic vulnerabilities and the broader institutional challenges facing fragile economies in East Africa.

- Conflict and Economic Disruption

Armed conflict has been one of the most significant obstacles to economic development in South Sudan. The destruction of infrastructure, displacement of populations, and disruption of productive activities have severely constrained economic growth. Research indicates that conflict has destroyed key infrastructure, including roads, bridges, hospitals, and schools, while also disrupting agricultural production and supply chains (Journal of Developing Country Studies, 2024; Acheampong & Enders, 2024). The displacement of more than 3.8 million people has weakened the labor force, reduced productivity across multiple sectors of the economy, and increased dependency on humanitarian assistance (Journal of Developing Country Studies, 2024; UNHCR, 2025).

Photo Credits: UN News

The economic losses associated with conflict are substantial. Multiple studies estimate that armed conflict has resulted in billions of dollars in economic losses due to reduced productivity, destruction of physical assets, and declining investment flows (Zhou & Hsiao, 2025; Akol, 2024). The destruction of economic infrastructure raises the cost of reconstruction and slows the pace of post‑conflict recovery, placing an additional burden on already fragile public finances (Collier et al., 2024).

Furthermore, persistent instability has significantly discouraged both domestic and foreign investment. In the absence of a stable political and security environment, businesses face heightened risks that constrain economic expansion and limit job creation. Post‑conflict countries such as South Sudan, characterized by weak governance structures and fragile economic fundamentals, are particularly vulnerable to external regional and global shocks (IMF, 2024). Disruptions in key sectors—such as energy and trade—have had severe consequences; for instance, interruptions in oil production have resulted in estimated revenue losses of approximately $7 million per day, further straining government finances and fiscal sustainability (World Bank, 2025b).

- Fiscal Policy, Taxation, and National Budgets

An examination of South Sudan’s fiscal framework reveals deep structural weaknesses in revenue generation and public financial management. Government revenue remains overwhelmingly dependent on oil, which accounts for around 90% of total government revenue and approximately 95% of exports (African Development Bank, 2023; IMF, 2024). This high dependence exposes the economy to external shocks, particularly fluctuations in global oil prices and regional disruptions affecting production and export routes.

Domestic revenue mobilization remains extremely limited. South Sudan’s tax-to-GDP ratio was estimated at approximately 4.1% in FY2022/23, with projections of about 5.8% in FY2023/24, making it one of the lowest in Sub-Saharan Africa (IMF, 2024). Moreover, non-oil revenues contribute less than 20% of the national budget, reflecting a narrow tax base and weak capacity for tax administration (World Bank, 2023). Key tax instruments such as value-added tax (VAT) contribute minimally, further highlighting structural inefficiencies in revenue collection.

On the expenditure side, fiscal data indicate volatility and weak budget credibility. Total government revenue declined from 34.7% of GDP in 2022/23 to about 26.5% in 2024/25, largely due to falling oil revenues, while expenditures remained relatively high at around 28–36% of GDP over the same period (IMF, 2024). This imbalance has contributed to recurring fiscal deficits and rising public debt, which is projected to reach approximately 48.6% of GDP in 2024/25 (IMF, 2024).

In addition to these structural constraints, persistent delays in the preparation and approval of national budgets have undermined fiscal discipline and effective public expenditure management. Weak transparency and governance challenges have further compounded the problem, with reports highlighting the mismanagement of significant public resources, including oil-backed financing arrangements (World Bank, 2025). These challenges disrupt service delivery, weaken development planning, and limit the government’s capacity to respond effectively to post-conflict reconstruction needs.

- Economic Exclusion and Persistent Poverty

Despite its natural resource wealth, South Sudan remains one of the poorest countries in the world. Poverty levels remain extremely high, reflecting deep structural inequalities and limited economic opportunities.

According to the South Sudan Poverty and Equity Assessment, approximately 92% of South Sudanese live below the national poverty line, while extreme poverty affects more than two-thirds of the population (World Bank, 2024). Poverty is particularly severe in rural areas, where most households depend on subsistence agriculture. Limited access to markets, poor infrastructure, climate shocks, and ongoing insecurity severely restrict agricultural productivity and household income (World Bank, 2024; ISS Africa, 2026).

Economic exclusion in South Sudan is also evident in limited access to education, healthcare, financial services, and formal employment opportunities (World Bank, 2025; Journal of Developing Country Studies, 2024). Weak institutions, governance challenges, and mismanagement of public resources have further constrained the equitable distribution of economic opportunities, entrenching inequality (World Bank, 2023; IMF, 2024).

Additionally, inequality in access to economic opportunities fuels social grievances and undermines national cohesion. Large segments of the population remain excluded from economic growth, increasing the risk of conflict and political instability (Radio Tamazuj, 2025; ISS Africa, 2026). External shocks—such as regional instability, disruptions in oil exports due to conflict in Sudan, or global geopolitical tensions affecting energy markets—further exacerbate vulnerability, limiting South Sudan’s capacity to achieve sustainable economic resilience (World Bank, 2025a; African Development Bank, 2023).

Addressing these challenges requires inclusive governance, strengthened institutions, and targeted investments in social services and rural development. Without these interventions, structural poverty, economic exclusion, and inequality are likely to persist, continuing to undermine South Sudan’s long-term development and stability (World Bank, 2024; ISS Africa, 2026).

- Public Expectations and Governance Challenges

While economic conditions remain difficult, public expectations for economic improvement continue to grow. Citizens expect the government to provide employment opportunities, infrastructure development, and access to essential services such as healthcare and education.

However, the government faces severe fiscal constraints that limit its ability to meet these expectations. South Sudan’s economy remains heavily dependent on oil revenues, which account for over 90 % of government revenue and the majority of export earnings (World Bank, 2021).

This heavy dependence on a single resource exposes the country to significant economic volatility. When oil production declines or prices fall, government revenues drop sharply, resulting in reduced public spending and delayed salary payments for public servants.

External shocks have also worsened economic conditions. For example, disruptions in oil export infrastructure linked to regional conflicts have led to significant fiscal crises and foreign exchange shortages. These challenges have contributed to inflation, food insecurity, and declining purchasing power among households (IMF, 2024). The gap between public expectations and government capacity to deliver services, therefore, continues to widen.

Photo Credit: FAO

- Structural Economic Vulnerabilities

South Sudan’s economic challenges are deeply rooted in structural vulnerabilities that limit long-term development.

First, the economy remains highly dependent on oil exports. Oil revenues constitute the majority of government income, making the country vulnerable to fluctuations in global commodity markets and geopolitical disruptions.

Second, economic diversification remains limited. Key sectors such as agriculture, manufacturing, and services remain underdeveloped due to insecurity, poor infrastructure, and limited access to capital.

Third, the country faces recurring humanitarian crises driven by climate shocks, flooding, and food insecurity. These crises place additional pressure on government resources and undermine household resilience.

Fourth, institutional weaknesses limit effective economic governance. Weak public financial management systems, corruption, and limited administrative capacity reduce the effectiveness of development policies.

Addressing these structural challenges is essential for building a resilient and inclusive economy.

- Conflicts and Regional Integration

South Sudan has gradually increased its economic integration with regional and international partners, thereby expanding trade opportunities but heightening its vulnerability to external shocks. As a member of the East African Community (EAC), South Sudan is economically linked with neighboring countries such as Uganda, Kenya, Ethiopia, and Sudan. While regional integration enhances market access and trade flows, it also exposes the country to the spillover effects of regional instability.

The ongoing conflict in Sudan has had particularly severe consequences for South Sudan’s economy. Since South Sudan relies on pipelines that run through Sudan to export its oil, the conflict has disrupted production and transportation, leading to significant declines in oil export revenues. Given that oil accounts for the bulk of government income, these disruptions have constrained the government’s ability to finance its national budget and deliver essential public services.

Beyond the region, South Sudan has in recent years strengthened its economic and strategic ties with Middle Eastern countries, including the United Arab Emirates, Saudi Arabia, and Qatar, particularly in the energy and investment sectors. While these partnerships provide important sources of capital and market access, they also increase the country’s exposure to global geopolitical dynamics.

In this context, conflicts in the Middle East—especially tensions involving the United States and Iran—could have significant economic implications for South Sudan. Such conflicts may trigger volatility in global oil prices, disrupt energy markets, and affect investment flows. For a fragile, oil-dependent economy like South Sudan, these external shocks could undermine economic resilience, exacerbate fiscal pressures, and negatively influence the country’s economic outlook for 2026.

- Policy Pathways for Inclusive Economic Recovery and Outlook

Achieving sustainable economic recovery in South Sudan requires a coordinated approach that integrates peacebuilding, economic reforms, and institutional strengthening. The following policy pathways are critical:

Durable Peace and Political Stability – Ensuring lasting peace and political stability must remain a top priority. Without a secure environment, key economic activities such as trade, agriculture, and investment cannot thrive, and public confidence in the state will remain low. Stability provides the foundation for rebuilding infrastructure, attracting investment, and enabling productive livelihoods.

Economic Diversification – Reducing dependence on oil revenue is essential. Investments in agriculture, infrastructure, and small-scale enterprises can broaden the economic base, enhance resilience, and generate employment. Improving agricultural productivity, in particular, can strengthen food security and provide income opportunities for rural populations, who represent the majority of South Sudanese households.

Transparency and Accountability in Resource Management – Effective and transparent management of natural resources, especially oil revenues, is critical. Prudent resource allocation can finance development programs, expand public services, and reduce opportunities for corruption that undermine public trust and fiscal stability.

Human Capital Development – Investment in education, healthcare, and vocational training is necessary to cultivate a skilled and healthy workforce capable of supporting long-term economic transformation. Strengthening human capital also enhances innovation and productivity across all sectors of the economy.

Institutional and Public Financial Management Strengthening – Strengthening public institutions, including fiscal management systems, enhances government capacity to plan, implement, and monitor policies effectively. Strong institutions are necessary for efficient service delivery, improved budget execution, and the creation of an enabling environment for private sector development.

By pursuing these interconnected policy pathways, South Sudan can foster inclusive economic recovery, build resilience to internal and external shocks, and create conditions for sustainable development and long-term stability.

- Conclusion

South Sudan’s economic and governance challenges are deeply intertwined with its history of conflict, institutional fragility, and structural economic dependence on oil. Despite significant natural resource endowments, the country has struggled to translate its wealth into inclusive growth, poverty reduction, and effective public service delivery. Persistent instability, weak fiscal management, and limited domestic revenue mobilization have further constrained the state’s capacity to meet growing public expectations.

This paper has shown that the interplay between conflict, economic exclusion, and governance deficits continues to undermine development efforts. Declining oil revenues, a narrow tax base, and recurrent delays in national budget processes have weakened fiscal stability and disrupted post-conflict reconstruction. At the same time, increasing regional and global economic integration—through membership in the East African Community and expanding ties with countries such as United Arab Emirates and Saudi Arabia—has exposed South Sudan to external shocks, including the spillover effects of conflict in Sudan and geopolitical tensions in the Middle East.

Addressing these challenges requires a comprehensive and sustained reform agenda. Strengthening public institutions, improving transparency and accountability in resource management, and broadening the domestic tax base are critical steps toward enhancing state capacity. Equally important is the need for economic diversification to reduce overreliance on oil and build resilience against external shocks. Moreover, ensuring that scarce public resources are allocated efficiently, transparently, and in a timely manner will be essential for restoring public trust and supporting long-term development.

Ultimately, sustainable peace and economic recovery in South Sudan will depend on the government’s ability to align public expectations with institutional capacity, foster inclusive governance, and create an enabling environment for investment and growth. Without these reforms, the cycle of fragility, economic decline, and unmet expectations is likely to persist, undermining the country’s prospects for stability and prosperity.

- References

Acheampong, T., & Enders, W. (2024). Conflict, infrastructure loss, and economic trajectories in fragile states. Journal of Peace Economics and Development.

Akol, L. (2024). Economic cost of conflict in South Sudan: Infrastructure, productivity, and investment. African Journal of Development Studies.

African Development Bank. (2023). South Sudan economic outlook 2023. African Development Bank Group.

Collier, P., Hoeffler, A., & Söderbom, M. (2024). Post conflict reconstruction and the economics of rebuilding. Oxford University Press.

EAC Secretariat. (2025). East African Community budget and fiscal reports 2023–24. EAC Secretariat.

International Monetary Fund (IMF). (2024). South Sudan: Staff-monitored program review and economic outlook. IMF.

Journal of Developing Country Studies. (2024). The impact of armed conflict on economic growth and sustainability in South Sudan.

Radio Tamazuj. (2025). 11 million South Sudanese faced extreme poverty in 2024 – report. Retrieved from https://www.radiotamazuj.org

United Nations High Commissioner for Refugees (UNHCR). (2025). South Sudan displacement report 2025. UNHCR.

World Bank. (2021). South Sudan economic update: Pathways to sustainable food security. World Bank.

World Bank. (2023). South Sudan economic monitor: Enhancing domestic revenue mobilization. World Bank.

World Bank. (2024). South Sudan poverty and equity assessment. World Bank.

World Bank. (2025a). South Sudan economic monitor: A pathway to overcome the crisis. World Bank.

World Bank. (2025b). South Sudan economic update: Urgent reforms for stability and growth. World Bank.

Zhou, X., & Hsiao, C. (2025). Conflict-driven economic losses in fragile economies. Journal of Conflict and Development.

Arita, S., Chakravorty, R., Kim, J., Lwin, W. Y., & Steinbach, S. (2026). Strait of Hormuz Closure and Global Fertilizer Trade Disruptions. NDSU Agricultural Trade Monitor, 2026(3), 1–26.

Reuters. (2026). Egypt’s energy import bill more than doubles as global prices surge. Retrieved March 18, 2026, from https://www.reuters.com/business/energy/egypts-energy-import-bill-more-than-doubles-global-prices-surge-2026-03-18/?utm_source=chatgpt.com

ISS Africa. (2026). South Sudan country profile — Poverty and inequality analysis. Retrieved from https://futures.issafrica.org/geographic/countries/south-sudan/?utm_source=chatgpt.com

Ms McDowell Juko, Chairperson East Africa Business Network (EABN): Elsa Juko-McDowell, a native of Uganda, is a remarkable individual with a deep passion for people and business. Her journey began in 2015 when she joined the East Africa Chamber of Commerce (EACC), an 18-year organization devoted to fostering trade and investments between the United States and East Africa, currently known as the East Africa Business Network. owns multiple businesses, including real estate development, investments, and consulting ventures. Additionally, Elsa serves as a North Texas District Export Council member. Can be reached

Ms McDowell Juko, Chairperson East Africa Business Network (EABN): Elsa Juko-McDowell, a native of Uganda, is a remarkable individual with a deep passion for people and business. Her journey began in 2015 when she joined the East Africa Chamber of Commerce (EACC), an 18-year organization devoted to fostering trade and investments between the United States and East Africa, currently known as the East Africa Business Network. owns multiple businesses, including real estate development, investments, and consulting ventures. Additionally, Elsa serves as a North Texas District Export Council member. Can be reached

Hon: Dr Abullah H Makame, Member of East Africa Legislative Assembly (EALA): Dr Makame, is a distinguished member of the East African Legislative Assembly (EALA) based in Arusha, Tanzania, where he is a commissioner and a former Chairperson of the Standing Committee in Agriculture, Environment, Tourism and Natural Resources. Dr Makame has served in various senior capacities in both the Government of United Republic of Tanzania and Zanzibar; academically, his docorate is from Birmingham UK and MSc from Strathclyde – Scotland, he holds a Professional Certificate in International Trade from Adelaide and has published both locally and internationally. Dr Makame serves in various boards across the EAC region. Can be reached via email:

Hon: Dr Abullah H Makame, Member of East Africa Legislative Assembly (EALA): Dr Makame, is a distinguished member of the East African Legislative Assembly (EALA) based in Arusha, Tanzania, where he is a commissioner and a former Chairperson of the Standing Committee in Agriculture, Environment, Tourism and Natural Resources. Dr Makame has served in various senior capacities in both the Government of United Republic of Tanzania and Zanzibar; academically, his docorate is from Birmingham UK and MSc from Strathclyde – Scotland, he holds a Professional Certificate in International Trade from Adelaide and has published both locally and internationally. Dr Makame serves in various boards across the EAC region. Can be reached via email:

Dr Kasirye Ibrahim, Executive Director, Economic Policy Research Centre (EPRC), Makerere University, Kampala: Uganda’s experience: Are government social interventions such as PDM working to shelter the poor and vulnerable against poverty?

Dr Kasirye Ibrahim, Executive Director, Economic Policy Research Centre (EPRC), Makerere University, Kampala: Uganda’s experience: Are government social interventions such as PDM working to shelter the poor and vulnerable against poverty? Mr Kwame Owino, Chief Executive Officer, Institute of Economic Affairs (IEA), Kenya: Can taxation be a solution and should we expect more taxes moving forward?

Mr Kwame Owino, Chief Executive Officer, Institute of Economic Affairs (IEA), Kenya: Can taxation be a solution and should we expect more taxes moving forward? Dr Mugisha Rweyemamu, Research Fellow, Economic Social Research Foundation, ESRF-Tanzania: Could Tanzania overtake its regional peers as the new regional economic giant?

Dr Mugisha Rweyemamu, Research Fellow, Economic Social Research Foundation, ESRF-Tanzania: Could Tanzania overtake its regional peers as the new regional economic giant? Hon: Zittto Kabwe, Economist and President of AcT-Wazalendo Political Party, Tanzania: What is totally wrong-Could we expect economic-political unrest amongst the youth-What should political actors do to avert a near economic catastrophe and social uprising (Azania Spring) similar to the famous Arab Spring. Is an economic inspired Azania Spring inevitable if things don’t change?

Hon: Zittto Kabwe, Economist and President of AcT-Wazalendo Political Party, Tanzania: What is totally wrong-Could we expect economic-political unrest amongst the youth-What should political actors do to avert a near economic catastrophe and social uprising (Azania Spring) similar to the famous Arab Spring. Is an economic inspired Azania Spring inevitable if things don’t change? Moses Kulaba, Convener, Governance and Economic Policy Centre

Moses Kulaba, Convener, Governance and Economic Policy Centre