Political Risk and Investment in EA: An Expose of violent tax protests and political risk on Trade and Investment in East Africa

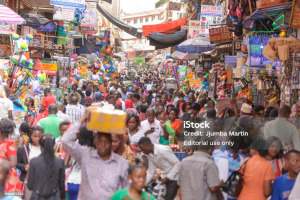

In our previous brief on Tax and Fiscal governance in East Africa, we observed that with dwindling foreign aid, it appears the governments in East Africa have resorted to squeezing everywhere to raise some dime. We cautioned that Taxation may be good however, when the extremes are beyond reasonableness, governments are bound to break their break the back of the economies they aspire to build[1]. The recent and ongoing tax protests that have rocked the East African regions, with violence and vandalism spiraling out of control in Kenya, clearly underscore this point. A failed tax administration and an irate society.

By Moses Kulaba, Governance and Economic Policy Centre

@taxjustice @politicalrisk

Freedom of expression, the right to picket and demonstrate and resist punitive taxation has been established over the years. The doctrine of no taxation without proper representation was long established by the Romans, Greeks and Americans during the famous Boston Tea Party 1773) and American war of independence, The French Revolution and the English, paving way into the famous Magna Carta.

This was further advanced by Adam Smith in his legendary Canons of Taxation asserting that generally, a good tax system must be underlined by proportionality and ability to pay[2] and political scientist Harold D Laswell’s tax law of who pays, what and when, and each individual or group should “pay their fair share. These principles that tax liability should be based on the taxpayer’s ability to pay is accepted in most countries as one of the bases of a socially just tax system and generally citizens are duty bound to reject a system that is regarded as unfair and disproportionally beyond their means[3].

However, when peaceful protests and demonstrations strategically drift towards violence, vandalism and murder like the ones we saw in Kenya, then these effectively transform into high level political risks to trade and investment.

According to multiple sources a political risk is a type of risk faced by investors, corporations, and governments that political decisions, events, or conditions will significantly affect the profitability of a business actor or the expected value of a given economic action. In simple terms, a political risk is the possibility that your business could suffer because of instability or political changes in a country: conflicts and unrest, changes in regime or government, changes in international policies or relations between countries, as well as changes that occur in a country’s policies, business laws or investment regulations[4]. Examples of political risks include; unilateral state decisions, war, terrorism, and civil unrest

By their nature, these risks are expensive to be insured against and constitute a major determinant factor for business in deciding where to invest or do business. Highly political risk countries experience sharp declines in investment and may attract low new trade and investments flows.

According to Trade and Investment experts such as Pierre Lamourelle, Deputy Global Head of Specialty Credit within Allianz Trade for Multinationals, the interconnected nature of the global economy makes it very possible that a political risk in one country may affect many businesses across the globe.

“What has changed in the 25 years since I started in this business is that we are living in a more connected world today,” says Pierre. On the upside, that means business is easier to conduct on a global scale. Almost everybody now has the ability to reach out to emerging countries or to conclude a contract and secure a sale in a foreign country.

On the downside, this means that when something goes wrong in one part of the world, you can feel the impact halfway around the globe – directly, if you are dealing with the country in question, or indirectly because of your diverse supply chain. Remember when the 20,000-ton container ship “Ever Given” got stuck in the Suez Canal in March 2021, shutting down international trade for a week?

In today’s increasingly interconnected world, “just-in-time” supply chains, global internet connection, and smartphones give SMEs the ability to conduct business in a global arena. This means the possibility for great opportunities, but also that every business is just steps away from political risk.

Persistent violent tax protests can make it difficult and unpredictable for the government to raise enough tax revenue to finance its obligations, including servicing of sovereign commitments such as paying off its debts and makes the economic environment very unpredictable. This can lead global economic and financial institutions to flag or down grade the Country’s economic status as risky , making difficult and more expensive for the country and companies to raise external capital for investment.

Moreover, the violent protests occurred or are happening at a critical period of the year when East African Countries such as Kenya record the highest number of tourist arrivals into the Country for the summer holiday. Before the protests, national parks, hotels and beaches in Kenya’s tourist hot spots had already recorded high tourist bookings and were expecting a bumper harvest this season as the global economies and travelers rebound from the COVID 19 lock down. Reports from multiple travel agents and hoteliers already indicate that most tourists have either cancelled or postponed their decisions to travel to Kenya and East Africa generally. Indeed, some already in the Country were gripped with fear of uncertainty and have left.

The burning image of an old plane at Uhuru Park did not send a good image either as most people around the world, unfamiliar with Kenya, thought Jomo Kenyatta International Airport was attacked and planes on the tarmac set on fire. A recorded video clip that trended on social media of passengers crammed up at JKIA with a voice note indicating that many were fleeing the country added salt to the pinch suggesting Kenya was not safe anymore!

Similarly, travel advisories have been issued to foreigners in country and intending to travel to Kenya, to do that if it is essential and be vigilant of their security as safety during this violent period cannot be guaranteed. With all these at play, Kenya may remain a blacklisted destination among some foreign tourists for some period to come, denying the country the much-needed foreign revenue and jobs in its service sector. At least a number of high conferences that were planned for Nairobi were cancelled.

The net effects of the demonstrations therefore go beyond having the bill rejected but have long-term economic effects on Kenya’s economy. The violent Gen-Z’s may have to reconsider their approach to avoid a full economic meltdown.

Of course, there are legitimate concerns that some current established large business and investments were already not providing benefits to the young people. Multiple reports have shown that some businesses were tax dodgers while others belong to the politically connected who used their political connections to shove deals and amassing wealth on the backbone of the majority Kenyans. Moreover, given the current loopholes in the governance systems, new trade and investment opportunities would not support or create many new economic opportunities either.

However, when these arguments are advanced, it is also imperative to look at the broader picture of the net effect that violent protests can have on Kenya’s economy and future that the Gen-Z seeks to address. Kenya’s economy is extensively connected and dependent on the global economy with most global business having chosen Nairobi as a regional financial hub. Violent demonstrations and disruption of such a magnitude can have significant long-term impacts.

With a government under siege and constrained with a debt tinkering on the margins of default and unrelenting rancorous youth roaming and burning the streets of Nairobi armed with negative social media, Kenya’s economy could slide into a free fall and recession, whose impacts on everyone could be far reaching.

Taxation and a strong tax system may contribute to improved governance through 3 maximum channels. Taxation establishes a fiscal social contract between citizens and the taxing state. Tax payers have a legitimate cause to expect something in return for paying taxes and are more likely to hold their governments to account. Governments have a stronger incentive to promote economic growth when they are dependent on fair taxes.

In this regard, we suggest the following;

- Resistance demonstrations and protests for tax rights must be expressed with limitations and restraint from both sides- The state and citizens alike

- Government must be rational when imposing taxes. Tax policies must be clear and predictable. Clearly, imposing taxes on bread and blanket exemption of choppers is a sign missed priorities.

- Government communication apparatus must be robust enough to explain to the citizens the justifications for taxation and the political class must lead by example demonstrating frugality in public expenditure.

- There must be distinction between private, public and national critical infrastructure, whose destruction may or can affect Kenya’s national security interest and state existence. Lest we forget, Kenya has been a victim of terrorism and still faces extensive threats from both internal and external elements, whose interests to harm Kenya has never wavered. Attacks on its critical infrastructure exposes the Country and Kenyans further to major threats.

- Re-engineering of Kenya’s governance and economy to address the contemporary needs for the Gen-Z. Times have changed and the Gen-Z who now constitute an overwhelming majority will effectively from 2027 be forever a major determinant of East Africa’s political future. Women will no longer be a game changer in electoral politics and outcomes but the Gen-Z will be.

- There is need for both political and social sobriety. East Africa needs good leadership and peace!

[1] Tax and Fiscal Governance: Is VAT milking the broken tax cow dry? An analysis of tax trends and impacts on EAC small traders, with a case of the recent traders’ demonstrations and boycotts in Uganda:

[2] Adam Smith, in his book, The Wealth of Nations, 1776

[3] Schronharl, K, etal; Histories of Tax Evasion , Avoidance and Resistance; https://library.oapen.org/bitstream/id/346cfc5f-6001-40e3-8a3b-fe46405df8c2/9781000823882.pdf

[4] https://www.allianz-trade.com/en_US/insights/what-is-political-risk.html#:~:text=Political%20risk%20is%20the%20possibility,country’s%20policies%2C%20business%20laws%20or

Dr Kasirye Ibrahim, Executive Director, Economic Policy Research Centre (EPRC), Makerere University, Kampala: Uganda’s experience: Are government social interventions such as PDM working to shelter the poor and vulnerable against poverty?

Dr Kasirye Ibrahim, Executive Director, Economic Policy Research Centre (EPRC), Makerere University, Kampala: Uganda’s experience: Are government social interventions such as PDM working to shelter the poor and vulnerable against poverty? Mr Kwame Owino, Chief Executive Officer, Institute of Economic Affairs (IEA), Kenya: Can taxation be a solution and should we expect more taxes moving forward?

Mr Kwame Owino, Chief Executive Officer, Institute of Economic Affairs (IEA), Kenya: Can taxation be a solution and should we expect more taxes moving forward? Dr Mugisha Rweyemamu, Research Fellow, Economic Social Research Foundation, ESRF-Tanzania: Could Tanzania overtake its regional peers as the new regional economic giant?

Dr Mugisha Rweyemamu, Research Fellow, Economic Social Research Foundation, ESRF-Tanzania: Could Tanzania overtake its regional peers as the new regional economic giant? Hon: Zittto Kabwe, Economist and President of AcT-Wazalendo Political Party, Tanzania: What is totally wrong-Could we expect economic-political unrest amongst the youth-What should political actors do to avert a near economic catastrophe and social uprising (Azania Spring) similar to the famous Arab Spring. Is an economic inspired Azania Spring inevitable if things don’t change?

Hon: Zittto Kabwe, Economist and President of AcT-Wazalendo Political Party, Tanzania: What is totally wrong-Could we expect economic-political unrest amongst the youth-What should political actors do to avert a near economic catastrophe and social uprising (Azania Spring) similar to the famous Arab Spring. Is an economic inspired Azania Spring inevitable if things don’t change? Moses Kulaba, Convener, Governance and Economic Policy Centre

Moses Kulaba, Convener, Governance and Economic Policy Centre