Re-Positioning women and gender concerns in Critical Green Transition Minerals: Should women be treated differently?

With the increasing focus on climate change and green transition minerals, multiple questions are asked whether women really matter and deserve to be treated differently.

Authors: Gloria Shechambo, Moses Kulaba and Judith Karangi, Governance and Economic Policy Centre

*We acknowledge valuable inputs from Ms Rachel Chagonja, CEO National Council of NGOs, Tanzania and Natural Resource Consultant

- Featured photo: Courtesy of IGF:https://www.igfmining.org/four-ways-empower-women-artisanal-small-scale-mining/

The mining sector has mostly been male dominated and has had a differential impact on how women have contributed and benefitted from the sector. Women in mining face multiple challenges including ownership to mining licenses, gender-based discrimination and earn less value from mining. Moreover, women have been traditionally the artisanal miners and dealers of what were considered less value minerals such as copper, gemstones and pearls. The global shift of interest towards cleaner energy has put a different demand on critical or transitional minerals such as tin, tungsten, has generated a new wave and venture by the rich into new territories, previously held by women and potentially exacerbating the problems that they already faced. (HakiRasilimali, 2021). There is already a rush by mining companies to take over land and acquire new licenses over land previously utilised by artisanal women. This shift could potentially lead to further inequalities and jeopardies the livelihoods of women in the sector (Pact World,2023).

This subject is essential at this point in time as it encourages governments to re-look into the state of women in critical minerals and how the new global shifts in the mining sector provide a different trajectory to small scale artisanal women miners in particular. Moreover, it is important because mining and transaction of critical/ transition minerals will be the ultimate development agenda of the next 30 years and is bound to affect Tanzania’s mineral governance landscape for the next foreseeable future (Kulaba,2022). Yet lopsided development without women, has always proven to be stagnant and unjust.

As Tanzania navigates the complexities of the energy transition, prioritizing gender inclusiveness in the mining sector will not only benefit women but also contribute to sustainable economic growth and development (BMZ, 2023).

What are Transitional Minerals

Critical, Green or Transitional Minerals are minerals that are considered vital in the support of the technology and industrial development required to support the global transition to clean energy. These minerals include but not limited to graphite, lithium, cobalt, copper, tungsten, tantalum etc. By virtue of their properties, these are slightly distinct from other conventional minerals such as gold and diamonds. According to global mining and energy reports the demand for critical green transition minerals will surge by many folds in the next decade as the global demand and countries race up towards reaching the Paris Agreement targets of Net Zero by 2050. Already Transition mineral rich countries such as the DRC, Zambia and Tanzania are experiencing a boom in global demand for mining licenses and opportunities for new investment. While this surge represents an opportunity for mineral rich countries, there is a likely risk that the benefits from this critical/ transition minerals booms could by pass women artisanal miners.

The intersection between Transitional Minerals and negative Gender biases

The mining sector has long been awash with negative gender biases, cultural norms, regulatory, systemic, structural and physical barriers towards women. Mining is considered a man’s task, hard and hazardous for women. Women by their physiological nature are not considered fit to enter tinny deep underground mining pits to extract minerals. In many African mining societies, it is culturally believed that minerals will disappear if women appear on the mining sites or enter the mining pits. Some studies (Kondo 2023) have shown that women have been forbidden to enter mines, that they themselves own for ‘safety’ concerns by local officials.

While some women groups have gone on to challenge these norms and participate in mining, their degree of participation may nevertheless be limited. Norms around domestic roles in the home, for instance, mean that while men can focus solely on mining, women must first complete chores in the home and agricultural activities before participating in mining activities, which limits their earning capacity and career progression. Women also tend to be less mobile, restricted to selling their minerals within mining areas where prices are lower, unlike men who sell their minerals beyond the mining area (Buss et al., 2017).

Moreover, the current legal and policy framework governing the extractive sector has not fully untangled these barriers and does not guarantee effective participation of women in the mining sector (Majamba ,2020). As a result, women have consistently played the less visible roles and are found towards the tail end of the extractives value chain occupying roles such as those of administrative support staff, informal laborers for food supply, sexual entertainment, cleaning services and those that are closest to extracting are artisanal miners.

Women constitute about 40-50% of Artisanal miners in Sub-Sahara Africa (Pact World, 2023); and dominantly involved in extracting minerals that were previously considered ‘less value minerals’ such as salt gemstones, pearls, iron, cobalt, copper, tin, tungsten and tantalum.

In brief, despite their numbers, women neither control ownership nor value of the mining sector. Without addressing these challenges, the emerging boom in Transition Minerals could reinforce the already existing parochial and restrictive barriers that hinder women in the mining sector, keeping women in abeyance from enjoying the economic benefits that come with transition minerals and mining generally for yet the next decades.

Despite their numbers and potential economic multiplier effects, women only own around 1% of all mining licenses and 6% of artisanal mining licenses in Tanzania. This must be a cause for alarm

Do existent shifts within the mining sector bring a different trajectory to women and artisanal miners?

The global agenda and discussions to mitigate negative effects of Climate Change and keeping global warming under 1.5 degree has brought a major shift towards energy transition, changed the mining landscape and upscaled the role of critical/green or transition minerals in Mining and development global policy discussions.

The shift provides both opportunities and risks not only to specific transition mineral rich countries but to women artisanal miners in particular (Policy Forum, 2022). Informed by the Paris Agreement Cop 21 adopted in 2015, the shift has significantly changed the global demand tending towards cleaner energy where critical minerals are needed as the raw materials. Critical minerals which are also called green minerals contribute to reducing unclean emissions for renewable technologies and are very essential for functioning of modern economies, technologies and industries including electronics, renewable energy, automobiles, aerospace and defense (BMZ,2023).

Moreover, the shift to critical minerals signifies a major change in global demand in minerals by super powers, rushing to secure critical supply chains and quantities needed to drive their clean energy industrial development and to secure their energy and strategic security needs.

For example, the demand for graphite and lithium has surged and the value for copper will increase for the next years to come. While this may be an opportunity, there is a risk that the developed countries are potentially bound to benefit more than supplier countries such as Tanzania.

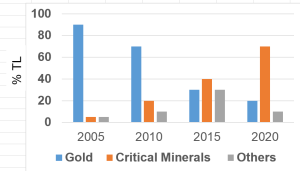

According to the Geological Survey of Tanzania and Mineral scoping reports (NRGI 2022) , Tanzania has close to 24 documented Critical Minerals occurrences and has witnessed a boom in new mining licenses. Over 50% of new mining licences issued between 2015 and 2020 targeted critical minerals. Tanzania has recorded new investments in Nickel and Graphite and exploration for large scale mining of Tungstein and Tantalum are underway. The government has placed attracting new investment in the critical minerals sector at the centre of its strategic investment drive for the next five years. A new or revised mining policy could be coming soon.

Figure 1: Tanzania Critical Minerals Exploration boom 2005-2020 (%TL = percentage of the total number of exploration licenses issued per annum) (Source: Tanzania Mining Commission and NRGI-Tanzania Scoping Study Report 2022)

Figure 1: Tanzania Critical Minerals Exploration boom 2005-2020 (%TL = percentage of the total number of exploration licenses issued per annum) (Source: Tanzania Mining Commission and NRGI-Tanzania Scoping Study Report 2022)

With the challenges already highlighted above, the new shift will not necessarily bring new unique challenges to artisanal small-scale miners and women in particular, however, on the more optimistic side, with increase in Foreign Direct Investment (FDI) can result into better labor market outcomes in the mining sector, infrastructural investment which will enable women and other ASMs to gain better access to market opportunities.

However, pertinent policy questions remain and solutions must be provided. For example, what specific changes in labor dimensions (e.g wages, decency in employment) are more favorable for women? What specific infrastructural needs are more specific and useful to women? And what do market opportunities look like exactly to women? This needs further dissection so as to cater them accordingly. With formalization of ASMs already underway, there might be a greater pressure by investors to ensure formalized ASMs also have access to legal protection against various forms of violations and more opportunities for skills development that is relevant to the sector. What specific skills distinct from male artisanal miners are needed for women? Being able to answer these questions intentionally would enable a more gendered impact to the envisaged developments without assumptions that positive effects would automatically trickle down to women.

With rising attention to responsible sourcing of critical minerals, there may be more attention to ensuring gender and social inclusion in the sector with standards more heightened. Economic empowerment is another potential area through which gender mainstreaming initiatives potential to the sector could be adopted. This may take a form of setting up women’s cooperatives, offering grants and expanding access to financial services to support women’s entrepreneurship in mining related engagements such as processing equipment(s).

A potential area for gender mainstreaming in mining is implementing mechanisms to support women in caring for their children after returning from maternity leave while working full-time in mining areas. For example, a study in Australia found that the proportion of women in the mining workforce was higher among those under 30 but declined significantly with age. This drop was partly attributed to the lack of a supportive environment, such as inadequate onsite childcare and family support systems (Weldegiorgis, 2022).

While Tanzania will have to balance between this development imperative and Climate Change obligations further risks on environmental, and local populations still remain detrimental. The intersection of women mining and energy transition needs a bigger attention and warrants to be assessed to ascertain specific economic opportunities, challenges and what the overall shift means to artisanal women.

Gaps and risks for missed opportunity

With such spurring potentials, come possible risks too. Most of ASMs and women who have been engaged in mining were operating without formal licenses on lands. Expansion of investment to critical minerals means further displacement by largescale companies where licenses might be granted to larger better resourced companies. This might present a larger land competition and worsen the economic situation of ASMs and poor women in the sector.

Technological divide between smaller and larger mining companies might further exacerbate the marginalization of small-scale miners and women as mining of critical minerals requires higher capital investment and advanced technology.

Environmental and health risks arising from large scale mining operations may cause further impacts on communities leaving women and poor artisanal miners prone to health risks due to their vulnerability and higher dependency on natural resources for livelihoods.

Last but not least, if larger inclusion polices are not carefully inculcated, gender inequalities in the mining sector may be furthered resulting in lesser opportunities for women to be in the formal mining and control of the mining sector and the value it provides.

Yet investment and increase of women in the critical minerals sector value chain has significant multiplier effects to the local economy. According the income expenditure studies, given their caregiving roles and geographical immobility limitations women have 10 times more chances of spending their income locally compared to men. In other words, incomes earned by women will create 10 times more economic benefits to the local economy compared to men.

A study in Zambia of some local businesses (groceries, clothing shops and bars) service in Mapatizya ASM sites indicated that on average, over 50 % of their customers were ASM workers and over 50 % of revenues also derived from ASM operators. The estimated percentage of female customers was 10–80 % with an average estimate of 48 % female customers. Local business owners felt that ASM increases cash flow into the local economy through purchase of largely consumer goods such as food, clothing, soap, kerosene and other essential household items. Studies in Tanzania’s mining areas has also confirmed similar patterns. Women also support other livelihood activities, e.g. farming and establishment of small micro-entrepreneurships and village saving and lending schemes.

With a total around 41,000 women constituting about 25-27% of the informal mining and artisanal sector in Tanzania, increasing this number can create up to 10 times multiplier effect on local household incomes, adding economic value and reducing poverty by significant folds.

Policy and Legal governance aspects

The legal and policy framework should provide the framework through which the government creates an enabling environment to enable a functional minerals’ sector along with ensuring women and artisanal miners’ increased involvement in the sector. Unfortunately, several literatures highlight the existing gaps in the legal and policy framework that hinder the effective involvement of women.

The legal framework governing the Mining Sector in Tanzania only responds partly to the challenges/barriers that women are facing. Despite the affirmative measures to recognize women in the mining sector through facilitating licensing for artisanal and small-scale miners (women included), the legal framework insufficiently supports the effective participation of women in the mining value chain especially in the most challenging areas namely capital skills and marketing (HakiRasirimali,2021).

The Mining Act of 2010 (amended in 2017) as the primary legislation governing Tanzania’s mining sector also manifests some gaps. Some provisions of the Mining Act was relatively more progressive in terms of ensuring gender parity in mining commission is at least 1/3 of the members must be women. The subsequent amendment in 2017 was rather regressive, where it provided that one out of two knowledgeable members should be a woman (Mjamba,2020). The Act does however not provide gender mainstreaming as a strategic tool of advancing women ownership and control of the mining sector.

The Extractive Industries Transparency Act (TEITA) requires for some disclosures on gender, however the extent to which women and ASM matters must discharged is not comprehensive. Moreover, the TEITA law was enacted with a mindset focus on conventional large scale mined minerals such as gold, tanzanite and diamonds. Critical Green Transition Minerals would be a new purview desiring a second look.

The Mining Act 2010 also includes local content requirements to Tanzanian nationals in employment and procurement however these provisions could be strengthened further by emphasizing the minimum threshold for the inclusion of women in jobs, entrepreneurship and service provision.

The Natural Wealth and Resources (Permanent Sovereignty) Act of 2017; the Natural Wealth and Resources Contracts (Review and Re-negotiation of Unconscionable Terms) Act of 2017; and, the Tanzania Extractive Industries (Transparency and Accountability) Act of 2015 are also not actively seeking to promote gender inclusiveness (HakiRasilimali,2020). These Acts have taken a value neutral approach to women and delegated their care to the state and the general public on ownership and governance matters.

In-terms of Land ownership challenge to women, the Tanzania Land Act (1999) and village Land Act (1999) recognize that women’s participation in mining is closely linked to the access and control over land. In this regard, the Act recognize women’s right to own lease and use land for productive purposes, however, customary practices still limit women’s access and control. Future amendments and reforms should consider incorporating gender aspects more explicitly by also mandating companies to adapt more gender sensitive policies and practices,

By loping women together with their male counterparts, the government assumes that these are equal players. It is oblivious of the historical challenges that women have faced and treats them like equal weights in boxing championship. The fact is that they are not. And should never be in this era of transitional minerals moving forward.

Recommendations to mitigate potential risks

- Government must review the existing legal framework with a futuristic woman in transition minerals lens. To ensure a more equitable benefit from this important upcoming energy transitional era, the Minerals legal framework would benefit from incorporating more stringent clauses that promote gender inclusiveness to protect women and artisanal miners in the Transition Minerals sector.

- Ring fence some mining licenses for critical green transition minerals to women and promote joint ventures between women miners and new transitional mineral companies.

- Formalization of mining licenses should take into consideration historical and structural barriers that small scale artisanal and women miners experience by providing access to financial credit and loans.

- Secure and strengthen women participation in transition minerals value chain. Economic empowerment interventions should continuously ensure a through gender impact analysis to asses who benefits more in the value chain and who is more affected negatively by the existent mineral operations. This goes along with identifying and providing relevant technical skills necessary for advancing women within the sector, narrowing the wage-gap, and enhancing markets.

- Women must deliberately create and government must support safe spaces for women in Transition Minerals. This must include efforts such as strengthening the Women in Mining Associations, formation of Tanzania Women Congress on Climate Change and Energy Transition and establishment of a dedicated National Symposiums and International Women Climate Conferences (COP) to consistently monitor and evaluate and discuss progress made by women in the critical minerals space.

-

For us at GEPC the formation and operation of a united women front in the form of a Women Congress on Climate Change and Energy Transition offers the only unique opportunity of breaking the barriers that have undermined the different women movements and mining associations, thereby unlocking the potential of women to influence the climate change and transitional minerals spectrum in a more coordinated and reinforced manner.

- Multinational Mining Companies must establish deliberate polices not to encroach or take over mineral licenses previously owned or occupied by women small scale and artisanal miners. Multinational Mining Companies must deliberately seek to partner with women miners as means for increasing women ownership and control of the Mining value Chain.

- Furthermore, enforce the law and practice to ensure larger mining companies do not encroach on women owned mining rights, reduce negative environmental impacts to communities and women in particular.

Conclusion

The global shift toward critical minerals presents a significant opportunity from critical or transitional mineral rich countries such as Tanzania. It however significantly creates both opportunities and risks for for women in artisanal mining. The booming demand could create an avalanche of new prospectors and investors targeting artisanal mining areas. Without targeted interventions, existing barriers—such as limited access to land, licenses, and financial resources—may further marginalize women in the sector. To ensure inclusive benefit for women in the critical minerals boom, , policy and legal frameworks must deliberately intentional to promote women’s participation through stronger protection, secured access to resources, and skills development. By addressing these challenges, Tanzania and other supplier countries can empower women artisanal miners and foster a more equitable and sustainable transition minerals sector. The vagaries of climate injustice can be addressed, the tainted history of the mining sector reclaimed and women catapulted into a better green future.

References

BMZ. (2023). Raw materials for energy transition. https://rue.bmz.de/rue-en/releases/157362-157362

- Buss, B. Rutherford, J. Hinton, et al. Gender and Artisanal and SmallScale Mining in Central and East Africa: Barriers and Benefits (2017), GrOW Working Paper No. 2

- Onditi. Gender Inequalities in Africa’s Mining Policies: A Study of Inequalities, Resource Conflict and Sustainability, Springer, Singapore (2022)

HakiRasilimali. (2021). Engendering the mining sector: To what extent are women benefiting or losing out on revenue management? https://www.hakirasilimali.or.tz/wp-content/uploads/2021/09/Engendering-the-Mining-Sector-in-Tanzania.pdf

Kondo, H. (2023) An exclusive look at Tanzanian women in mining xxxxxxxxxx. https://www.sciencedirect.com/science/article/pii/S2214790X24000595

Majamba, H. I. (2020). The gender gap in Tanzania’s mining sector. Tanzania Journal of Development Studies, 18(1), 29-40.

Pact World. (2023). Artisanal miners: A hidden but critical force in the global economy. https://www.pactworld.org/blog/artisanal-miners-hidden-critical-force-global-economy

Policy Forum. (2022). Critical minerals and energy transition in Tanzania: A new dance, maybe?https://www.policyforum-tz.org/blog/2022-06-14/critical-minerals-and-energy-transition-tanzania-new-dance-maybe

The Citizen. (2023). How to bridge the gender gap in mining. https://www.thecitizen.co.tz/tanzania/magazines/woman/how-to-bridge-gender-gap-in-mining-4549718

United Republic of Tanzania Ministry of Minerals. (2024). Transforming Tanzania’s mining sector with strategic minerals on cards. https://www.madini.go.tz/page/e8a4201d-286f-4409-9db0-719311652336

Weldegiorgis, F (2022). Women and the Mine of the Future: A gendered analysis of the Employment and Skills in the Large-Scale Mining Sector -Australia

A study by Ahmed et al in 2017 suggested that Tanzania has an annual technical solar power potential in Tanzania was estimated to be 31,482 TWh for CSP technology and 38,804 TWh for PV technology. Potential solar energy resources are found in the central parts of the country

A study by Ahmed et al in 2017 suggested that Tanzania has an annual technical solar power potential in Tanzania was estimated to be 31,482 TWh for CSP technology and 38,804 TWh for PV technology. Potential solar energy resources are found in the central parts of the country Tanzania has areas of high onshore wind potential that cover more than 10% of its land

Tanzania has areas of high onshore wind potential that cover more than 10% of its land