Authors: Moses Kulaba and Roger Vutsoro, Governance and Economic Policy Centre

This short analytical study explores the existing national, regional and global certification mechanisms such as the Kimberly Process, ICGLR, OECD Due diligence measures, Responsible Mining Initiatives in the quagmire of improving of minerals governance. It entangles and assesses the increasing perceptions (based on evidence from countries such as the DRC) that the current certification regime is running dangerously obsolete, not designed for critical minerals and thus needs a review and realignment for new purpose, including proposing measures that go beyond the current regional certification.

Decades ago, mineral certification was mooted as a solution to addressing the chronic problems of illegal mining, mineral smuggling and mineral driven conflicts, economic injustices and impunity in mineral rich countries. To this regard, regional and global mineral certification mechanisms were developed with countries and mining companies required to sign up to these new certification principle and mechanisms. However, decades after, minerals continue to be drivers of conflict and harm in many countries.

As the appetite for Critical or Transitional minerals required for the green and clean energy industrial technology gains gusto momentum, there are concerns that this new mineral dash may exacerbate corruption, conflict and suffering in critical minerals rich countries. Apart from calls to establish regional value chains, there is evidence to suggest that a proper global certification mechanism should be put in place to ensure responsive sourcing of critical minerals and that their extraction does not lead to further harm.

What is mineral certification

Mineral certification is a process that verifies the origin and legitimacy of minerals, ensuring they are not associated with conflict or human rights abuses. It involves tracing minerals from the mine site to the final point of export and confirming they are free from illegal activities. This helps to prevent the financing of armed groups and other illicit activities linked to mineral extraction. This certification involves a thorough verification process to trace the minerals’ origin and verify they are free from illegal financing, armed group involvement, and human rights abuses.

At face value, this sounds like a good measure, however existing mechanisms of a similar nature such as the Kimberly process, ICGLR certification initiative and the OECD Due diligence measures have not succeeded in fully addressing the issue of conflict minerals and mineral smuggling. In Countries such as the Democratic Republic of Congo and Mozambique, minerals continue to be a driver of conflict and mineral smuggling to neighboring countries is still rife. This therefore puts to question the efficacy of the existing global certification mechanism in strengthening governance, regulating supply, improving ethical mining business conduct and reducing harm from extractive resources.

Existing major Regional and Global Mineral Certification regimes

The Kimberly Process Certification System (KPCS)

The Kimberly Process (KPCS) is a global standard certification process established in 2003 by the United Nations General Assembly (Under resolution 55/56) to prevent conflict diamonds from entering the mainstream diamond market. KPCS was set up to ensure that diamonds as precious minerals are sourced and traded in a responsible manner, reducing financing conflicts and human rights violation. KPCS has laid out requirements for participating member countries to comply including[1]

- Enforcement of regulatory standards to control export and import of rough diamonds

- Principles of transparent practices to ensure integrity of the diamond supply chains

- Selective trading with only KP certified and compliant members

- Verification of exports to ensure every traded diamond is accompanied by a conflict free certificate.

Member countries are obliged to enforce these standards. To date 60 participants (representing 86 countries) are signatory members to the Kimberley process and have committed to applying KP principles in the certification of its traded diamonds. The standards require that;

- Participant countries must enforce stringent legal and regulatory standards to control the import and export of rough diamonds and ensure adherence to KP requirements.

- Participants commit to transparent practices, which are crucial for the integrity of the diamond supply chain, by exchanging accurate and timely statistical data.

- Trade is permitted only between certified KP members who comply fully with these international standards, safeguarding the legitimacy of the diamond trade.

- Every diamond export is closely inspected and must be accompanied by a valid KP certificate, certifying that the diamonds are conflict-free to prevent the entry of illicit stones into the market.

National Level Governance and Implementation of the Kimberly Process; A case of Tanzania

In Tanzania the Kimberly Process Office is situated in the Mining Commission, an Institution within the Ministry of Minerals. This office is responsible for the implementation of the KPCS activities, import and export of rough diamond; the office is under the authority of the Executive Secretary. The Mining Commission works closely with the Tanzania Revenue Authority’s Customs Department, Tanzania Intelligence and Security Service and the Police Force for strengthening internal control. The Kimberley Process Office forms a part of the Mineral Audit and Trade Department, which is under the Director for Mineral Audit and Trade who assists the Executive Secretary in administering the KPCS activities. The office issues Annual reports.

Before the issuance of Kimberley Process Certificate, the exporter of rough diamonds must submit a valid Dealer’s license/Mining license, which allows him to export minerals outside Tanzania. The Dealer’s license indicates full address, type of minerals, the premises and signature of Executive Secretary or a person authorized to sign. The exporter fills the application form which indicates license type, license number, weight, value, source of diamonds to confirm that diamonds are conflict free, place of export and declaration of exporter by putting his/her signature, name and qualification to apply for a certificate and pays to the government USD 100 as an application fee for Kimberley Process certificate. Post to the valuation process, the exporter is required to pay royalty (6% of a value) and inspection fee (1% of value) to the Government.

Any person who contravenes any of the provision in Diamond trading regulation commits an offence and liable: In case of an individual to imprisonment for a term not exceeding three years or to a fine not exceeding US dollar twenty thousand (US$ 20,000) or to both. In case of body corporate, to a fine not exceeding US dollar one hundred thousand (US$ 100,000), or c. Cancelation of his license and permanently be disqualified from prospecting, mining or dealing in diamond and any other minerals. Any rough diamonds obtained contrary to the provisions of Diamond trading regulations shall be forfeited in addition to other penalties[2].

The International Conference on Great Lakes Region (ICGLR) Mineral Certification Measures

The ICGLR Certification mechanism was developed to address the persistent of mineral driven conflicts in the Africa Great Lakes region. It aims to create a conducive environment for cooperation among member states while also ensuring the protection and well-being of the people living in the Africa Great Lakes region.

The ICGLR Certificate confirms a mineral shipment is conflict-free and meets the ICGLR’s ethical sourcing standards, ensuring it’s free from illegal influence and responsibly traced from mine to market. This certification involves a thorough verification process to trace the minerals’ origin and verify they are free from illegal financing, armed group involvement, and human rights abuses. It provides buyers with the assurance that the minerals meet ICGLR requirements for transparency, legality, and responsible sourcing, supporting ethical supply chains in the region[3].

Currently the DRC, Uganda, Kenya, Rwanda and Burundi are members to the ICGLR’s certification mechanism. Mineral flows are analyzed via an ICGLR Regional Database, using the data on individual shipments collected and transmitted to the ICGLR by each Member States. The database is verified annually via ICGLR Third Party Audits. The mechanism is viewed as an important regional standard and tool for enhancing collaboration, transparency, and development in Africa’s Great Lakes region, promoting accountability and encouraging businesses to pursue certification for adherence.

The OECD Due Diligence Guidance for Responsible Mineral Supply Chain

Requires that company supply chains of all minerals from conflict affected and high-risk areas, must respect human rights and avoid contributing to conflict through their mineral or metal purchasing decisions and practices. Recognizes that trade and investment in natural mineral resources hold great potential for generating income, growth and prosperity, sustaining livelihoods and fostering local development. However, a large share of these resources is located in conflict affected and high-risk areas. In these areas, exploitation of natural mineral resources is significant and may contribute, directly or indirectly, to armed conflict, gross human rights violations and hinder economic and social development[4].

The OECD Due Diligence Guidance is considered as the first example of a collaborative government-backed multi-stakeholder initiative on responsible supply chain management of minerals from conflict-affected areas. Its objective is to help companies respect human rights and avoid contributing to conflict through their mineral sourcing practices[5].

The Guidance is also intended to cultivate transparent mineral supply chains and sustainable corporate engagement in the mineral sector with a view to enabling countries to benefit from their mineral resources and preventing the extraction and trade of minerals from becoming a source of conflict, human rights abuses, and insecurity. With its Supplements on Tin, Tantalum, Tungsten and Gold, the OECD Guidance provides companies with a complete package to source minerals responsibly in order for trade in those minerals to support peace and development and not conflict[6]

Responsible Minerals Initiative

The Responsible Minerals Initiative (RMI) is a voluntary membership body of companies and industry players with a vision to ensure that mineral supply chains contribute positively to social economic development globally. It seeks to promote the common goal of understanding and contributing to mitigating the salient social and environmental impacts of extraction and processing of minerals in supply chains. It leverages partnerships and use of international standards such as the United Nations Guiding Principles on Business and Human Rights or the OECD Due Diligence Guidance as our guideposts[7].

Comprised of more than 500 member companies; the Responsible Minerals Initiative is considered one of the most utilized and respected resources for companies from a range of industries addressing responsible mineral sourcing issues in their supply chains. RMI provides companies with tools and resources to make sourcing decisions that improve regulatory compliance and support responsible sourcing of minerals from conflict-affected and high-risk areas. RMI undertakes due diligence, assurance and reporting templates for cobalt, gold, tin, tungsten, tin, tantalum and other minerals.

The Nexus between Critical Minerals, Conflict and Harm

There is a strong connection between the extraction and trade of certain minerals and the exacerbation of armed conflicts and instability in various regions, particularly in developing countries. Globally, critical minerals fueling Green Tech are also fueling conflict[8] Armed groups often exploit the demand for these minerals (like tin, tantalum, tungsten, and gold, collectively known as “conflict minerals”) to fund their operations, including the purchase of weapons[9]. This reliance on minerals to fuel conflict can lead to human rights abuses environmental degradation, and social unrest, hindering sustainable development.

Critical minerals such as bauxite, manganese cobalt, lithium and uranium have fuelled conflicts in the DRC, Guinea, Niger, Mali, Chad and Central Africa Republic[10] Myanmar has also experienced a post-coup rush for control over its rare earth minerals, while Latin American countries like Chile and Colombia are grappling with how to ensure that their lithium wealth benefits local economies rather than multinational corporations[11].

Critical Minerals and conflict; A case for DRC

Multiple reports produced by UN and Civil society show that the ongoing violence in the DRC is linked to mineral extraction, with rebel insurgents motivated by a desire to extract from the region’s vast cobalt and coltan reserves. Since the onset of the infamous second Congo War in 1998, control over the DRC’s vast mineral resources has fuelled conflict between armed groups and militias. These factions fight over mining territories, using profits from the illegal extraction and smuggling of conflict minerals to finance their operations and purchase weapons. The struggle for control over mineral-rich areas has led to prolonged violence, contributing to the deaths of millions and leaving entire regions destabilized[12].

In the DRC, according to the UN Group of Experts, the M23 established control over the mineral-rich area and created a new transportation route to Rwanda. Through taxation and smuggling of minerals, the armed group is financially benefiting from DRC’s mineral resources. It’s estimated that the group is receiving approximately $800,000 USD monthly from the production and trade of minerals at Rubaya.

While some mine sites in eastern DRC may not be directly affected by the conflict, early 2025started with violence in Goma (a major mineral export and transit hub), as well as insecurity moving towards South Kivu with recent clashes in in Nyabibwe, a mineral rich area known for 3Ts and gold, located halfway between Goma and Bukavu. As of mid-February, the M23 had occupied Bukavu, another major mineral export and transit hub in the region.

Recent reports also indicate armed groups in Ituri Province are forming alliances with the M23, while new violence in the province has sparked worries of a larger regional conflict. The UN Group of Experts estimated that armed groups based in Ituri Province generated approximately $140 million USD in 2024, dwarfing the illicit revenue generated by 3Ts[13] Other armed militias and groups such as Allied Democratic Forces (ADF) are equally benefiting from the loot.

In light of this reality, the abundance of critical minerals offers a potential opportunity for economic wellbeing but the geopolitics and the dash for their control and extraction has potential of increasing conflicts in Africa[14] According to Global witness, the extraction and trade of some critical minerals is intensifying new geopolitical tensions and reinforcing long-standing patterns of exploitation[15] including conflicts.

The Trump Ukraine deal revealed a connection of critical minerals to the Russia and Ukraine war and how natural resources in Ukraine have become a key bargaining chip in international diplomacy between the US and Russia. In the same perspective, the US and the Democratic Republic of Congo are close to sign a minerals-for-security deal, highlighting the increase role of critical minerals in geopolitics and conflict.

In fact, the government of the Democratic Republic of Congo reached out to the Donald Trump administration with a Ukrainian-style proposal in February 2025 in response to the rapid advance of the Rwandan-backed M23 rebel group in the east of the country. The U.S. government has responded enthusiastically with a flurry of negotiations aimed at ending a decades-long conflict born out of the Rwandan genocide of 1994.

The political momentum is building towards a potential peace deal between Congo and Rwanda to be accompanied by bilateral minerals deals between both countries and the United States. At stake are the mineral riches of North and South Kivu provinces, a major but highly problematic source of metals such as tin, tungsten and coltan[16].

According to different sources, this deal once signed could boost Rwanda processing of Congo minerals and provide the US with an assured source of processed critical minerals required to support its industrial technology and security needs.

Gaps and why a new regime for mineral certification is required

The existing major regional and global mineral certification regimes have significant gaps that necessitate that a new regime is developed.

- Narrowness in focus and scope: Existing certification mechanisms such KP are narrow in scope largely target diamonds and were not designed to cover a broader mining sector. The ICGLR covers the 3Ts and gold. The emergency of a wider list of critical minerals adds a new context which the KP and ICGLR certification mechanisms were not designed for.

- Voluntary mechanisms; The existing mechanisms are largely voluntary and member states companies encouraged to join and comply with the standards. For instance, the 21st meeting of the CIRGL Regional Committee on the fight against the illegal exploitation of natural resources recommended CIRGL Secretariat to compile a comprehensive report on the status of implementation of the six tools of the regional certification mechanism. This report revealed that the Republic of Rwanda has not yet established the traceability chain for gold. Instead, Rwanda controls gold extraction and trade using conventional methods and does not issue ICGLR certificates for gold exports[17].”

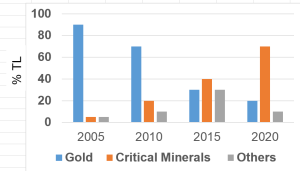

- Limited in geographical and legal scope: For instance, the OECD Due diligence Guidance is largely applicable to companies from OECD member countries but with limited enforcement mechanisms in non-OECD countries. Yet mining companies from non-OECD Countries such as China are emerging as the leading exploiters of Africa’s critical minerals according to WTO reports[18]. from the DRC. Chinese based companies own or operate 80 percent of the critical mineral production in the DRC, much of which is sent to China for processing for export via the global supply chain[19] Moreover the ICGLR is confined to its member states while the RMI covers only its 500 members.

-

- Illicit smuggling and trading in conflict minerals continue despite the presence of current certification mechanisms. For instance, despite its membership to the Kimberley Process (KP) and ICGLR commitments, Tanzania’s diamond sector is reported as facing entrenched governance challenges: opaque supply chains, smuggling, and minimal community benefits. Tanzania’s diamonds have suffered from environmental concerns, price volatility from synthetics and smuggled diamonds from regional conflicts areas[20].

Moreover, critical minerals including diamonds are smuggled across borders, transacted in established commercial capitals and hubs such as Kigali, Kampala, Nairobi and Dubai. For instance, a Global Witness investigation report indicates that an international commodities trader Traxys bought conflict coltan smuggled from Democratic Republic of Congo (DRC) to Rwanda[21] The investigation revealed that the multibillion-dollar company headquartered in Luxembourg bought 280 tonnes of coltan from Rwanda in 2024 based on customs documents seen by Global Witness.

Analysis by Global Witness of trade data and testimonies from two coltan smugglers suggested that a big share of the coltan Traxys bought from Rwanda was connected to the ongoing war in the east of DRC. African Panther’s coltan exports soared to unprecedented volumes in 2024, exceeding the combined total of the export volumes recorded over the previous four years. This increase in exports coincided with the escalation of the war in North Kivu and increased smuggling of conflict coltan from Rubaya, further suggesting that an important share of African Panther’s 2024 exports was smuggled from conflict zones in DRC[22].

Despite having limited or no known deposits and operational mines, some countries in East Africa and the Middle East have emerged as leading exporters of critical minerals such as cobalt, lithium and coltan. Study reports show large volumes of critical minerals transacted via East Africa to foreign markets such as the UAE and China[23]. For instance, in 2025 Kenyan authorities intercepted 10 containers of suspected smuggled copper at the port of Mombasa[24] These illicitly acquired, smuggled and transacted minerals have found market into the UAE and Western capitals in Switzerland and New York. In 2023 alone, Kenya’s exports of copper to the United Arab Emirates were valued at US$22.27 million. The UAE exports mineral products, including critical minerals, in significant quantities, primarily to Japan, China, and India.

- Ongoing critical minerals driven conflicts and the rise of new geopolitical conflicts in producer countries: The ongoing mineral driven conflicts have already been documented in the cobalt, coltan mineral rich Eastern DRC and elsewhere but the rush for securing access and control of mineral supply chains by superpowers is reviving geopolitical interests and may result in new geopolitical conflicts.

In the Democratic Republic of Congo (DRC), for instance, since the revision of its mining law in 2018, the country has attracted no responsible Western investors in the mining industry. Meanwhile, China has come to dominate the production of cobalt and copper, primarily mined in the Katanga and Lualaba regions. The recent re-negotiation by the Tshisekedi Administration of the imbalanced minerals-against infrastructure deal signed in 2008 under the Kabila administration between the DRC and China was perceived by China as triggered by the United State of America.

Aware of the security and economic implications of China’s control over the DRC’s critical minerals supply chain, the United States has signaled its return to the DRC mining sector through the recent acquisition of Australian AVZ Minerals’ assets in the Manono Lithium Project by KoBold Metals. In addition, the U.S. is committed to funding the Lobito Corridor—a strategic railway project essential for transporting critical minerals from the Central African Copperbelt to Western markets.

Through its International Development Finance Corporation (DFC), the U.S. has pledged a $550 million loan to support the Lobito Corridor. This project is considered vital in countering Chinese influence in the region by providing an alternative route for exporting critical minerals. This plea was reiterated in Luanda/Angola in January 2024 by the former US President, John Biden, during his last visit to Africa as an US President, in presence of both Angola and DR Congo Presidents.

The corridor is viewed as part of the Partnership for Global Infrastructure and Investment, a G7 initiative aimed at competing with China’s growing presence on the continent. While the Lobito project is designed to challenge Chinese dominance, both Western and Chinese firms will be allowed to use the infrastructure it provides. This dual-access approach raises questions about its strategic value, particularly under a US administration led by President Donald Trump, whose priority is competition with Beijing. The Lobito Corridor railway could be a physical indicator of the resuscitated geopolitical rivalry and convergence of global superpowers on the African continent as a source for critical mineral resources.

Failure to implement due diligence and traceability mechanisms

During the OECD conference on responsible minerals supply chain held in May 2024 in Paris, many Congolese civil society organizations raised concern over the increasing failure in the implementation of due diligence standards in the DRC. CSO mentioned that private sector actors have failed to fully implement supply chain due diligence in alignment with international standards, most notably the OECD Due Diligence Guidance for Responsible Minerals Supply Chains from Conflict-Affected and High-Risk Area. IMPACT added that companies are either turning a blind eye, preferring not to ask questions about the source of their purchases, or have been complicit by over relying on industry schemes despite red flags being raised in UN Group of Experts reports.

The concern around ITSCI—the sole traceability and due diligence provider for 3Ts in DRC—has been so great that in 2024 it lost its recognition with the Responsible Minerals Initiative (RMI), with RMI noting that important gaps remained in the scheme’s fulfilment of recognition terms. Despite this move, the UN Group of Experts has expressed concern that many private sector actors still rely on the scheme to conduct due diligence without carrying out additional independent quality controls required by international standards[25].

Civil Society Call for reforms

Because of these gaps civil society organisations have constantly urged for a review and development of a new certification mechanism regime, expanded and aligned to emerging context of transition minerals. For instance, at the start of the 2025 KP plenary in Dubai the Civil Society Coalition pointed out the gaps of the KP in addressing the challenges of diamond mining, smuggling and poverty in the Central African Republic[26]. CSO observed that the KP was narrow in focus, limited to diamonds and the imposed conflict diamond embargos had targeted smugglers without protecting the diamond mining communities.

The KP does not—and likely will not soon—prevent diamonds from being associated with issues outside the narrow conflict diamond definition, including human rights abuses, violence by public and private security forces, forced labour, and environmental degradation. Rigorous due diligence is essential, yet it remains insufficiently addressed.

For instance the KP in Central Africa Republic’s (CAR) experience demonstrated that the sole existence of the certification scheme does not make diamond governance exemplary. Though diamonds share similar governance challenges with other minerals, the Kimberley Process has largely remained isolated from broader dialogues on mineral-related due diligence.

Civil society demanded for the need to bridge the gaps in the KP certification mechanism by inter alia increasing transparency and engagement with mining communities. CSOs argued that without transparency, the KP will never effectively achieve its mandate of conflict prevention.

Moreover, the existing certification mechanisms are criticized as elitist, disconnected from the community needs and blind to social economic injustices. For example, the KP certification mechanism does not cover the extent to which the mining of the diamond minerals has benefited the communities from where they are sourced.

Investigations by the Kimberly Process Civil Society Coalition of mining operations in Sierra Leone, Lesotho, and the Democratic Republic of Congo, reveals the often-ignored consequences of large-scale diamond mining on local communities in African countries[27].

In Tanzania, despite mining diamonds for more than 100 years, Shyinyanga remains amongst the poorest remains the poorest region in the country[28]. The critical minerals rich Eastern DRC provinces of Kasai Oriental, Kasai Central, North and South Kivu are among the poorest and least developed in the world.

For diamond resources to truly benefit communities, the documentary identifies greater transparency and independent monitoring as key elements to enhance corporate accountability. Mining companies, industry actors and states all have a role to play to protect community rights and improve both mining and sourcing practices[29].

Further, certification mechanisms do not sufficiently cover or protect citizen against state excesses and inspired violence. Yet the very atrocities committed by rebel groups, which led to the KP’s creation in 2003, are now mirrored by certain governments and their security forces. Top ranking government officials and security forces in the Eastern DRC have been accused of being complacent to illicit mineral trade. The military junta in Myanmar is accused of widespread human rights violations including killings of civilians in critical mineral rich village areas in Kayah state closer to the Thailand border[30].

Conclusion

While certification mechanisms such as the Kimberly process were established for a major purpose of controlling blood diamonds over the years, they have this role to an extent but equally shown inherent gaps and shortcomings. Their limitation in scope, involuntary membership nature and poor implementation is a major limitation. They were set up when diamond was among the top most traded commodity and driver of conflicts in countries such as Angola, Liberia and Siera Leone. With the increasing surge in demand for critical minerals such as Nickel, Cobalt, Coltan, Graphite, Lithium, Tin Tungsten and Rare Earth Elements, the new frontiers mineral driven conflicts have expanded and cannot continue to remain on diamonds. In the current and future context, it will be untenable for critical minerals to remain outside the purview of mineral certification. For the existing certification mechanisms to be relevant and fitted for the changing context and era of energy of transition, substantive reviews and reforms are required.

Recommendations for future certification mechanisms

- Expand the KPI and ICGLR certification to cover a broad range of critical minerals or develop a new commensurate certification measure for critical minerals, with a focus on ethical sourcing, conflict and governance.

- Pay attention to the ongoing problems in mining such as the environmental concerns in critical minerals mining operations and their contribution to social and ecological harm to communities and countries from where they are sourced.

- Pay close attention to ongoing issues within critical minerals supply chains, including human rights abuses, armed conflicts, the fair distribution of benefits to local communities, and compliance with national labor laws

- Review the existing mineral audit standards, blend constitution of audit teams with experts, civil society and community representatives to increase transparency and integrity in certification

- Require exporting countries to demonstrate significant economic presence of the critical mineral commensurate with export volumes.

- Impose export embargoes and critical mineral trading sanctions on countries or companies involved in perpetrating smuggling and export of illicitly acquired and conflict critical minerals.

- Expand the scope of existing certification mechanisms such as the Kimberly process to capture community benefits from diamonds and critical minerals.

- Demand that membership to regional and global certification and tracking mechanism must be mandatory for all critical minerals producing and exporting countries

- Countries that produce critical minerals should diversify their investors and pursue win-win partnerships to prevent their territories from becoming geopolitical battlegrounds for superpowers competing for access to these resources in the era of energy transition

- Enhance public database and reconciliation system for tracking mineral flows to better balance production, purchases, and exports at various levels (exporters, mines, mining regions, and Member States).

- To maximize the benefits from critical mineral supply chains, producer countries should prioritize investments that add value to minerals and promote local content. This approach will generate more jobs for millions of unemployed youths, stimulate economic growth, and facilitate technology transfer and reduce susceptibility to conflict

References

Aikael Etal (2021) Understanding poverty dynamics and vulnerability in Tanzania: 2012–2018 available at https://onlinelibrary.wiley.com/doi/10.1111/rode.12829 accessed on 15 May 2025

Martin A, etal (2014), All that Glitters is not Gold: Dubai, Congo and the illicit trade of critical minerals, Partnership Africa Canada, May 2014

Andy Home, After Ukraine deal, US turns its critical minerals gaze to Africa, available at https://www.reuters.com/markets/, accessed on May 22

Global Witness (2025) available at https://globalwitness.org/en/press-releases/new-investigation-suggests-eu-trader-traxys-buys-conflict-minerals-from-drc/ accessed on 15 May 2025

IMPACT, Actors Must Suspend Sourcing Minerals Financing Armed Groups in Democratic Republic of Congo, available at https://impacttransform.org/, accessed on May 23, 1:46pm

ICGLR, Report on the Status of Implementation of the Six Tools of the ICGLR Regional Initiative on Natural Resources in Member States, P14

ISSD (2018) Green Conflict Minerals; The Fuels of conflict in the transition to a low carbon economy; available at https://www.iisd.org/story/green-conflict-minerals/ accessed on 15 May 2025

Panzi Foundation available via https://panzifoundation.org/conflict-minerals-and-sexual-violence-in-the-drc/# accessed on 15 May 2025

The African Climate Foundation Report; Geopolitics of Critical Minerals in Renewable Supply Chains available at https://africanclimatefoundation.org/wp-content/uploads/2022/09/800644-ACF-03_Geopolitics-of-critical-minerals-R_WEB.pdf accessed on 15 May 2025

The Eastleigh Voice (2025); Police launch investigation into suspected copper smuggling at Mombasa port; available at https://eastleighvoice.co.ke/business/112007/police-probe-suspected-copper-smuggling-at-mombasa-port accessed on 15 May 2025

US International Finance Cooperation https://www.dfc.gov/investment-story/strengthening-critical-mineral-supply-chains-countering-chinas-dominance#:~:text=But%20critical%20mineral%20supply%20chains,sent%20to%20China%20for%20processing.

WTO (2024): High demand for energy-related critical minerals creates supply chain pressures; available at

Online sources

[1] https://www.kimberleyprocess.com/about/what-is-kp

[2] The United Republic of Tanzania: Mining Commission; A Report on implementation of the Kimberly Process Certification Scheme for Tanzania Year 2023

[3]ICGLR; available via https://icglrcertification.com/ accessed 13 May 2025

[4]OECD Report (2016) available via https://www.oecd.org/en/publications/oecd-due-diligence-guidance-for-responsible-supply-chains-of-minerals-from-conflict-affected-and-high-risk-areas_9789264252479-en.html, accessed on 13 May 2025

[5] OECD (2016), OECD Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas: Third Edition, OECD Publishing, Paris, https://doi.org/10.1787/9789264252479-en.

[6] ibid

[7] https://www.responsiblemineralsinitiative.org/

[8] https://www.worldpoliticsreview.com/critical-minerals-conflict-eu/

[9] European Commission: Trade and Economic Security, Conflict Minerals regulation available at https://policy.trade.ec.europa.eu/development-and-sustainability/conflict-minerals-regulation_en#:~:text=In%20politically%20unstable%20areas%2C%20armed,mobile%20phones%2C%20cars%20and%20jewellery. Accessed on 15 May 2025

[10] ISSD (2018) Green Conflict Minerals; The Fuels of conflict in the transition to a low carbon economy; available at https://www.iisd.org/story/green-conflict-minerals/ accessed on 15 May 2025

[11] ibid

[12] Panzi Foundation available via https://panzifoundation.org/conflict-minerals-and-sexual-violence-in-the-drc/# accessed on 15 May 2025

[13] IMPACT, Actors Must Suspend Sourcing Minerals Financing Armed Groups in Democratic Republic of Congo, available at https://impacttransform.org/, accessed on May 23, 1:46pm

[14] The African Climate Foundation Report; Geopolitics of Critical Minerals in Renewable Supply Chains available at https://africanclimatefoundation.org/wp-content/uploads/2022/09/800644-ACF-03_Geopolitics-of-critical-minerals-R_WEB.pdf accessed on 15 May 2025

[15] Global Witness; Critical Minerals Fuel Conflicts available via https://globalwitness.org/en/campaigns/transition-minerals/the-critical-minerals-scramble-how-the-race-for-resources-is-fuelling-conflict-and-inequality/#:~:text=How%20are%20critical%20minerals%20driving,communities%20in%20resource%2Drich%20nations. Accessed on 15 May 2025

[16] Andy Home, After Ukraine deal, US turns its critical minerals gaze to Africa, available at https://www.reuters.com/markets/, accessed on May 22

[17] ICGLR, Report on the Status of Implementation of the Six Tools of the ICGLR Regional Initiative on Natural Resources in Member States, P14

[18] WTO (2024): High demand for energy-related critical minerals creates supply chain pressures; available at https://www.wto.org/english/blogs_e/data_blog_e/blog_dta_10jan24_e.htm#:~:text=Exports,all%20at%206%20per%20cent). Accessed on 15 May 2025

[19] US International Finance Cooperation https://www.dfc.gov/investment-story/strengthening-critical-mineral-supply-chains-countering-chinas-dominance#:~:text=But%20critical%20mineral%20supply%20chains,sent%20to%20China%20for%20processing.

[20] URT: Ministry of Minerals, Mining Commission; A Report on implementation of the Kimberly Process Certification Scheme for Tanzania Year 2023

[21]Global Witness (2025) available at https://globalwitness.org/en/press-releases/new-investigation-suggests-eu-trader-traxys-buys-conflict-minerals-from-drc/ accessed on 15 May 2025

[22] ibid

[23] Martin A, etal (2014), All that Glitters is not Gold: Dubai, Congo and the illicit trade of critical minerals, Partnership Africa Canada, May 2014

[24] The Eastleigh Voice (2025); Police launch investigation into suspected copper smuggling at Mombasa port; available at https://eastleighvoice.co.ke/business/112007/police-probe-suspected-copper-smuggling-at-mombasa-port accessed on 15 May 2025

[25] IMPACT, Actors Must Suspend Sourcing Minerals Financing Armed Groups in Democratic Republic of Congo, available at https://impacttransform.org/, accessed on May 23, 1:46pm

[26] https://www.kpcivilsociety.org/activity/kimberley-process-lifts-ineffective-embargo-end-of-an-era-for-the-central-african-republic-and-another-clear-signal-that-conflict-diamond-scheme-needs-serious-fixing/

[27] Kimberly Civil Society Coalition (2025); BEYOND SHINING ILLUSIONS: New documentary exposes the unspoken realities of large-scale diamond mining available at https://www.kpcivilsociety.org/press/beyond-shining-illusions-new-documentary-exposes-the-unspoken-realities-of-diamond-mining-in-african-countries/ accessed 15 May 2025

[28] Aikael Etal (2021) Understanding poverty dynamics and vulnerability in Tanzania: 2012–2018 available at https://onlinelibrary.wiley.com/doi/10.1111/rode.12829 accessed on 15 May 2025

[29] ibid

[30] https://www.dw.com/en/myanmar-land-mine-use-amounts-to-war-crimes-amnesty-report/a-62533770