Young people are the majority of Tanzania’s population , destined to inherit the future yet are seriously at a risk of climate change. Many are actively engaged in mitigation measures such as tree planting campaigns with limited focus on the policy and practical measures that are required to ensure or determine a fossil free future is achieved. Effective youth participation in SDGs and NDCs is a goal that is still far from reach.

Author: Arafat Bakir Lesheve, SDG Ambassador and Junior Associate, Governance and Economic Policy Centre

# Featured photo image source: African Climate and Environmental Centre-AFAS

# Click here to register for the forthcoming webinar on implementation of SDGS and NDCs in Africa scheduled for 31st October 2024 via the Link: https://us06web.zoom.us/meeting/register/tZYodOCsqTsuEt1URomW6I9uz6IjSyzq5S96

The transition to a fossil-free future is crucial for Tanzania to achieve sustainable development and combat climate change. The United Nations has set several targets for achieving a fossil-free future by 2030 and 2050. These targets aim to enhance international cooperation in the fight against climate change, promote clean energy research and technology, reduce reliance on fossil fuels, reduce greenhouse gas emissions and speed up the transition to clean and renewable sources of energy.

In 2021 Tanzania developed its Nationally Determined Contributions (NDCs), which spells out how the government plans to build resilience against climate change and contribute to clean future. The NDC is anchored on delivering a fossil free future by 2050 yet the document and its implementation has remained largely a technical exercise with limited knowledge and participation of young people.

Many young people are actively engaged in mitigation measures such as tree planting campaigns with limited knowledge, focus, engagement and participation in the policy and practical measures that are required to ensure or determine a fossil free future is achieved. With the youth comprising over 65% of Tanzania’s total population, engaging and empowering young people will be crucial to the success of these national and global targets.

This short brief exposes the opportunities , gaps and the need for an intentional repurposing of Tanzania’s youth in climate change and the implementation of the NDC along with the Sustainable Development Goals (SDGs) so as to achieve a fossil free future by 2030 and 2050.

Climate Change and a fossil free future in Tanzania

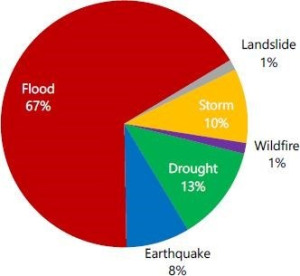

Despite being among the least polluters, Tanzania is seriously affected by climate change. The country has experienced irregular rainfall patterns, extended droughts, floods and deforestation. Currently, a significant proportion (about 70%) of all types of natural disasters in Tanzania are climate change related and are linked to recurrent droughts and floods.

The most recent projections for climate change in Tanzania (Future Climate for Africa, 2017)9 show a strong agreement on continued future warming in the range of 0.8°C to 1.8°C by the 2040s, evenly distributed across Tanzania. The warming trend leads to a corresponding increase in the number of days above 30°C by 20-50 days in the central and eastern parts and up to 80 additional days in the coastal area of Tanzania. Warming until 2090 is projected in the range of 1.6°C to 5.0°C depending on the level of greenhouse gases in the atmosphere[1]

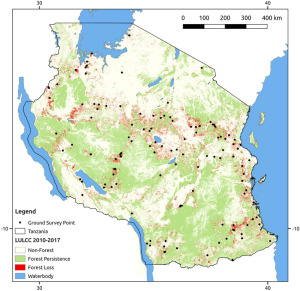

Moreover, climate change’s impact on Tanzania’s forest cover and sensitive ecosystems has been increasing. According to reports, Tanzania’s forest cover has reduced by at least one third over the past decade, thereby reducing the coverage of the natural carbon sink that has protected us for generations. Annually, almost 38% of Tanzania’s forest cover is being lost at the rate of about 400,000 ha annually and should this continue, the country would deplete its forest cover in the next 50-80 years[2].

Figure 1: Map of forest loss in Tanzania during 2010–2017 and location of ground survey points

Figure 1: Map of forest loss in Tanzania during 2010–2017 and location of ground survey points

The extreme weather patterns affect National Economic growth due to large dependence of Tanzania’s Growth Domestic Product (GDP) on Climate sensitive activities such as agriculture. The recent floods affected crops and farmland while the extended droughts in some regions have increased food insecurity and poverty by almost half. Sensitive ecological and biodiversity systems hosted within from forests and wooded areas are affected and climate related diseases such as malaria in previously cold and less malaria prone regions such as Moshi, Arusha, Lushoto, Iringa and Mbeya are on the increase.

According to medical reports, malaria is a major public health problem in mainland Tanzania and a leading cause of morbidity and mortality, particularly in children under five years of age and pregnant women. Moreover, the climate condition has become favourable for transmission throughout almost the entire country, with about 95% of mainland Tanzania at risk.

Over the past few years Tanzania now has the third largest population at risk of stable malaria in Africa after Nigeria and Democratic Republic of the Congo[1]. Clearly, there is a nexus between climate change and the social-economic and public policy challenges that Tanzania faces.

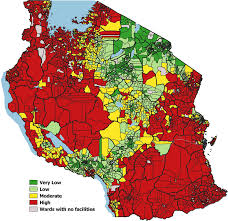

Figure 2: Malaria Prevalence in Mainland Tanzania 2017-2019: Source: Research Gate

The UN’s perilous search for a fossil free future

The UN under the Agenda 2030 targets to achieve a fossil free future by reducing global greenhouse gas emissions by half by 2030 and to achieve net zero by 2050.

For this to be feasible the world has to gradually transit from the use of fossil-based fuels towards renewables and clean energy sources. Fossil fuels, such as coal, oil and gas, are by far the largest contributor to global climate change, accounting for over 75 percent of global greenhouse gas emissions and nearly 90 percent of all carbon dioxide emissions.

Therefore, ramping up investment in alternative sources of energy that are clean, accessible, affordable, sustainable, and reliable offers a way out of the enormous climate change challenges that we face. To achieve this requires a radical shift in global energy system but equally collective participation. The UN has encouraged countries to develop and implement Sustainable Development Goals (SDGs) and Nationally Determined Contributions (NDCs), as road maps towards a sustainable cleaner future, yet many countries like Tanzania face a bumpy road ahead. The underfunding and limited meaningful participation by the youth is holding back success.

Climate Change, SDGs and the Nationally Determined Contributions (NDC) in Tanzania

In line with the UN Paris Agreement and call to climate action, the Tanzanian government set targets for climate change response and achieving a fossil-free future. The government aims to accelerate mitigation and adaptation measures, cutting Green House Emissions and contributing towards a transition to cleaner and renewable sources of energy.

These targets are clearly stipulated in Tanzania’s National Adaptation Plans (NAPs), National Climate Change Response Strategies (NCCRS) and most recently the Nationally Determined Contributions (NDC) in 2021. The NDC provides a set of interventions on adaptation and mitigation which are expected to build Tanzania’s resilience to the impacts of climate change and at the same time contribute to the global efforts to reduce greenhouse gases.

According to the NDC, the government commits to reduce greenhouse gas emissions economy-wide between 30- 35% relative to the Business-As-Usual (BAU) scenario by 2030. The NDC further indicates that about 138-153 million tons of Carbon dioxide equivalent (MtCO2e)-gross emissions is expected to be reduced depending on the baseline efficiency improvements, consistent with its sustainable development agenda.

The NDC goals are aligned to the UN Sustainable Development Goals (SDCs) 2015, in particular SDG13 and other closely related goals such as SDG (1.7,12,14,15.16 &17). They further in synchrony with the Agenda 2063 on the Future of Africa We want and the Sendai Framework on Disaster Risk Reduction (2011).

To achieve these targets, the government commits to consider the impacts of climate change in development planning at all levels and to pursue adaptation measures as outlined in the NDC. Despite these efforts, many SDG targets are off course and NDC’s implementation has been slow. The NDC implementation is faced with financial, governance, institutional and participation gaps, which are delaying or may ultimately thwart its successful achievement of a climate safe and fossil free future.

Gaps in Climate Change, NDC and SDG implementation

The Economics of climate change and implementation of SDGs and the NDC for a climate safe and fossil free future is proving to be an expensive affair.

According to The Economics of Climate Change reports for Mainland Tanzania (2011) and Zanzibar (2011) , an initial cost estimate of addressing current climate change risks is about USD 500 million per year[2]. These reports provide indicative costs for enhancing adaptive capacity and long-term resilience in Tanzania. This cost is projected to increase rapidly in the future, with an estimate of up to USD 1 billion per year by 2030[3].

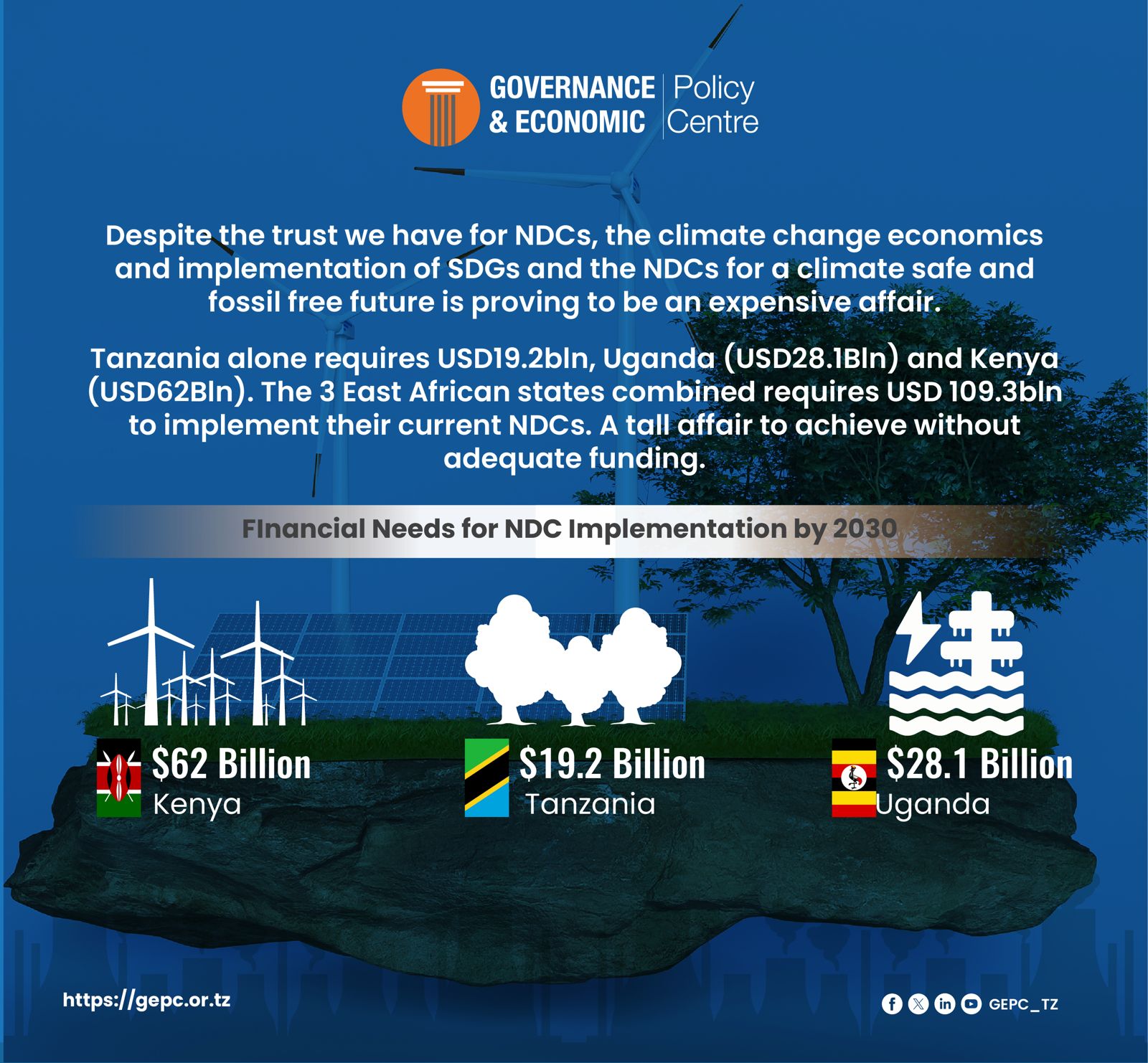

Further, the net economic costs of addressing climate change impacts are estimated to be equivalent to 1 to 2% of GDP per year by 20305. Similarly, Tanzania would require an investment of approximately USD 160 billion for mitigation activities aimed at achieving 100% renewable energy for electricity, buildings, and industry by 2050[4]. In total the NDC estimates that USD19,232,170,000 is required for its full implementation.

Moreover, Tanzania is facing several challenges related to weak institutional, financial constraints, poor access to appropriate technologies; weak climate knowledge management, inadequate participation of key stakeholders, and low public awareness have significantly affected effective implementation of various strategies, programmes, and plans[5]

The government has identified an institutional and governance framework for implementation. This includes the National Steering Committees and National Technical Committees for Mainland Tanzania and Zanzibar. It further mentions the need for mainstreaming intervention but conspicuously, misses listing or identifying the youth as key stakeholders in this implementation.

With tweaks to its current policy and practice landscape, by purposefully targeting involvement of more young people, we believe, Tanzania’s achievement of its SDGs targets and climate change and energy transition goals as elaborated in the NDCs and overall National Development Plans could be faster

Tanzania’s road towards a fossil free future

In 2014 the per capita emissions of the United Republic of Tanzania were estimated at 0.22 tCO2e[1] . This was significantly below global average of 7.58 tCO2e[2] recorded in the same year. However, given the disproportional effect of climate change, adaptation to the adverse impacts continues to be a topmost priority in the implementation of the NDC.

Tanzania underlines the importance of harnessing opportunities and benefits available in mitigating climate change through pursuing a sustainable, low-carbon development pathway in the context of sustainable development. Thus, the NDC takes into account global ambition of keeping temperature increase well below 2°C as per the Paris Agreement.

Moreover, Tanzania is aiming for a greater use of natural gas and harnessing renewable energy sources to reduce on emissions. There are an estimated 57 trillion cubic feet of discovered reserves of which to-date over 100 million cubic feet have been exploited to produce 527 MW10. The government acknowledges that whilst natural gas is a fossil fuel, and therefore contributes to increasing climate change, it results in half the CO2 emissions as charcoal

Currently the government of Tanzania aims to shift away from biomass and increase the share of renewable energy sources such as hydro, wind, and solar in its energy use mix. Tanzania’s energy sector is currently dominated by traditional biomass; accounting for more than 82% of the total energy consumption as of 2019. As of 2022 energy usage in households, charcoal and wood represented 87% of the energy used, Liquefied Petroleum Gas (LPG) accounted for 10%, and other sources such as electricity accounted for about 3%[3].

Secondly, Tanzania has an estimated hydro potential of up to 4.7GW. However, as of 2021, only 573.7 MW (around 12%) of hydro capacity had been installed. The government plans to further develop its hydro capacity to increase the share of renewable energy.

Thirdly, while Tanzania aims to increase its renewable energy generation, there are also plans to ramp up investment in natural gas and coal. The government aims to reach 6700MW (33%) from natural gas and 5300MW (26%) from coal by 2044. However, further investments or reliance on fossil fuels such as coal and natural gas is considered as an energy transition risk as the country may lock itself into a high carbon-intensive pathway and thereby running contrary to achieving the NDC goals.

Furthermore, Tanzania has significant deposits of critical minerals that are considered essential for the clean energy transition. These minerals include nickel, graphite, copper, lithium, and others. The demand for these minerals expected to increase as clean energy technologies develop. This presents an opportunity for Tanzania to benefit from their extraction to value addition hence powering the global transition to a green economy.

The youth dividend and missed opportunities for climate change, NDCs and SDGs in Tanzania

Globally, the youth represent a significant portion of the population and their active involvement and engagement in supporting government and UN targets are essential. According to Tanzania’s 2022 census reports, the youth (under 35 years) constitute significant proportion (over 60%) of Tanzania’s population. They account for the largest active labour force of the population and no doubt have potentials to bring about economic growth and development of the country. Moreover, the demographics and dynamics of youth have changed substantially over the last decade. Many young people are highly educated and technologically exposed and skilled. They are a dividend waiting to be utilized in many respects.

The implementation of Tanzania’s NDC is supposed to be guided by the principles of the UNFCCC, particularly the principle of equity and that of common but differentiated responsibilities and respective capabilities. Furthermore, the implementation is supposed to be implemented in a transparent and participatory manner in accordance with the provisions of the Paris Agreement. Despite these principles, the youth are yet to be fully engaged and harnessed for climate change and a fossil free future.

Since 2006 government has made efforts by developing the National Climate Adaptations Programs and the National Climate Change Strategy. However, Tanzania does not have a climate change policy and its practical engagement of youth despite the numbers has been quite fragmented.

Despite the major progress made, very limited deliberate and structured youth engagement opportunities have been created. For example, there is a government initiative on clean cooking targeting women but is not clear what role the youth can play in this campaign. Moreover, the Youth Policy is not aligned with the Climate Change and Energy policy. The NDC for example is very silent on youth and mentions these in generic terms lobed together under the gender considerations. Governance challenges and weak intra-government coordination exists. There is weak insufficient capacity and resources for youth to engage.

To date, this potential of Tanzania’s youth participation, in the context of the global climate change is largely limited or focused on climate mitigation while engagement in energy transition discourse towards a fossil free future has been substantively low.

How can youth be repurposed for climate change, SDGs and NDC implementation for a fossil free future?

There are collective actions that Tanzanian youth can uptake to support government plans and UN targets for SDGs, NDCs and a clean future by 2030 and 2050. These includes actions such as creating a facilitative environment, investment in advocacy, awareness creation, skills development, creating of innovations, movement mobilization, partnership and collaboration for the goals. Tanzanian youth possess the energy, innovation, and sense of urgency required to drive the transition to a fossil-free future. By leveraging their skills and passion, young people can play a vital role with multiple entry points as below.

1. Promote education amongst youth on SDGs and NDCs in Tanzania

As indicated, despite the good intentions and targets set in the Sustainable Development Goals (SDGs and the Nationally Determined Contributions (NDCs), these goals and documents remain largely unknown to youth and young people in Tanzania. Deliberate efforts to popularize them can ramp up youth uptake and support in their implementation.

2. Raise Awareness and Advocate for Renewable Energy:

Towards achieving this, the youth and other stakeholders, including the government should organize awareness campaigns and workshops to educate youth about the benefits of renewable energy and the negative impacts of fossil fuels. As the population continues to grow, so will the demand for cheap energy, and an economy reliant on fossil fuels is creating drastic changes to our climate; Investing in solar, wind and thermal power, improving energy productivity, and ensuring energy for all is vital if we are to achieve SDG 7 by 2030.

Tanzania Youth led organizations must be supported to amplify the voices of Tanzanian youth in advocating for a transition to renewable energy. Engage in advocacy efforts to promote renewable energy policies and initiatives at the local, national, and international levels;

2. Promote Energy Efficiency and Conservation

Tanzanian youth can organize campaigns and workshops to raise awareness about the importance of energy efficiency and conservation. They can educate their peers and communities about the benefits of using energy-efficient appliances, reducing energy consumption, and adopting sustainable practices.

Dr. Samia Suluhu Hasan the President of the United Republic of Tanzania is a global champion of clean cooking solutions that aims to address over reliance on toxic biomass, gender inequality against women as well as reduce impact of climate change. Tanzania’s youth should be in frontline to promote clean cooking solution with the country.

For the government to support youth roles is key to encourage energy-efficient practices among youth by promoting energy-saving habits in households, schools, and communities. Youth and youth led organizations should be supported to advocate for the implementation of energy-efficient infrastructure and appliances in public spaces and buildings.

NGOs, and government agencies must collaborate with energy experts to develop engaging and interactive training materials that cater for the needs and interests of young people towards promoting energy efficiency.

3. Advocating for policy changes

Advocating for policy changes is a crucial step in promoting renewable energy and climate action. Tanzanian youth have the opportunity to actively engage with local and national government representatives to push for policies that support renewable energy and discourage the use of fossil fuels.

Through outreach to their government representatives, youth can express their concerns about climate change and the need for renewable energy policies. They can request meetings or participate in public forums to discuss the importance of transitioning to renewable energy sources and highlight the benefits it can bring to the environment and the economy. By sharing their knowledge and experiences, youth can help policymakers understand the urgency of taking action on climate change and recognize the potential of renewable energy.

Additionally, youth-led organizations and initiatives focused on climate action must provide a platform for young people to come together and advocate for sustainable policies.

4. Engage in Sustainable Agriculture and Land Use

Tanzania youth must be supported to engage in sustainable agriculture and land use. Engaging in sustainable agriculture is of paramount importance in promoting environmental conservation and reducing reliance on fossil fuel-based inputs in farming practices. Tanzanian youth have a significant role to play in actively supporting and advocating for sustainable farming methods that prioritize organic techniques, agroforestry, and permaculture.

5. Foster Entrepreneurship and Innovation in Renewable Energy

Support young people to engage in entrepreneurship and renewable energy. Participating in green entrepreneurship presents Tanzanian youth with exciting prospects to contribute to the sustainable energy sector while establishing their own businesses. By developing innovative solutions for energy efficiency and conservation, young entrepreneurs can make a positive impact on the environment and contribute to the country’s economic growth.

6. Engaging in waste management practices

Promoting environmental sustainability and mitigating the harmful effects of waste necessitate active engagement in waste management practices. Tanzanian youth can play a vital role by championing recycling, composting, and waste reduction initiatives within schools, communities, and households.

By raising awareness about recycling’s significance and providing resources for proper waste separation, the youth can redirect recyclable materials away from landfills, thus fostering a circular economy. Moreover, they can advocate for composting as an effective means of minimizing organic waste while generating nutrient-rich soil for gardening and agriculture. Through their enthusiastic involvement in waste management, Tanzanian youth can contribute significantly to creating cleaner and more sustainable communities and a brighter future for the environment.

Conclusively, Tanzania’s road towards a fossil free future has so far been bumpy and marked with commitments and challenges. Tanzania however has opportunities amongst its youthful population and can turn up the tide to ride faster towards net zero.

References

[1] National Climate Change Strategy, Vice President’s Office, United Republic of Tanzania.

[2] Emissions Database for Global Atmospheric Research (EDGAR), Joint Research Centre (JRC).

[3] ibid

[1] https://web-archive.lshtm.ac.uk/www.linkmalaria.org/country-profiles/tanzania.html

[2] The Economics of Climate change in the United Republic of Tanzania, January 2011

[3] Ibid

[4] URT; Tanzania’s Nationally Determined Contributions, 2021

[5] URT; Tanzania’s Nationally Determined Contributions, 2021

[1] URT: Tanzania Nationally Determined Contribution, 2021

[2] https://dicf.unepgrid.ch/united-republic-tanzania/forest

Ms McDowell Juko, Chairperson East Africa Business Network (EABN): Elsa Juko-McDowell, a native of Uganda, is a remarkable individual with a deep passion for people and business. Her journey began in 2015 when she joined the East Africa Chamber of Commerce (EACC), an 18-year organization devoted to fostering trade and investments between the United States and East Africa, currently known as the East Africa Business Network. owns multiple businesses, including real estate development, investments, and consulting ventures. Additionally, Elsa serves as a North Texas District Export Council member. Can be reached via: info@eabn.co or chairman@eabn.co

Ms McDowell Juko, Chairperson East Africa Business Network (EABN): Elsa Juko-McDowell, a native of Uganda, is a remarkable individual with a deep passion for people and business. Her journey began in 2015 when she joined the East Africa Chamber of Commerce (EACC), an 18-year organization devoted to fostering trade and investments between the United States and East Africa, currently known as the East Africa Business Network. owns multiple businesses, including real estate development, investments, and consulting ventures. Additionally, Elsa serves as a North Texas District Export Council member. Can be reached via: info@eabn.co or chairman@eabn.co Mr. Adrian Njau, Ag. Executive Director, East African Business Council: Adrian Njau is the Executive Director of the East African Business Council (EABN), the apex advocacy body of private sector associations and corporates from the 7 East African Community (EAC) Partner States (Kenya, Democratic Republic of the Congo, Tanzania, Rwanda, Burundi, Uganda and South Sudan). Adrian holds a Master’s Degree in International Trade and a Bachelor’s Degree in Economics, both obtained from the University of Dar es Salaam. His academic background is complemented by professional certifications and specialized training in trade, investment, policy and regional integration from Switzerland, Singapore, and Sweden, among others. With over two decades of experience, Adrian has been instrumental in research and policy at the Chamber. Can be reached via: Email: info@eabc-online.com

Mr. Adrian Njau, Ag. Executive Director, East African Business Council: Adrian Njau is the Executive Director of the East African Business Council (EABN), the apex advocacy body of private sector associations and corporates from the 7 East African Community (EAC) Partner States (Kenya, Democratic Republic of the Congo, Tanzania, Rwanda, Burundi, Uganda and South Sudan). Adrian holds a Master’s Degree in International Trade and a Bachelor’s Degree in Economics, both obtained from the University of Dar es Salaam. His academic background is complemented by professional certifications and specialized training in trade, investment, policy and regional integration from Switzerland, Singapore, and Sweden, among others. With over two decades of experience, Adrian has been instrumental in research and policy at the Chamber. Can be reached via: Email: info@eabc-online.com Mr Robert Ssuna, International Trade and Tax Expert, Researcher and Consultant, Governance and Economic Policy Centre: Robert is an Independent Consultant on Tax Trade and Investment. He is Chartered Economic Policy Analyst (CEPA), a Fellow of the Global Academy of Finance and Management with over 15 years of experience in economic policy analysis focusing on tax, trade, and investment at national, regional, and global levels. He is also a member of the Base Erosion Profit Shifting (BEPS) Monitoring Group. Prior to this, he served as a Supervisor Research Statistics and Policy Analysis in the Research and Planning Division of the Uganda Revenue Authority. Can be reached via: ssuunaster@gmail.com

Mr Robert Ssuna, International Trade and Tax Expert, Researcher and Consultant, Governance and Economic Policy Centre: Robert is an Independent Consultant on Tax Trade and Investment. He is Chartered Economic Policy Analyst (CEPA), a Fellow of the Global Academy of Finance and Management with over 15 years of experience in economic policy analysis focusing on tax, trade, and investment at national, regional, and global levels. He is also a member of the Base Erosion Profit Shifting (BEPS) Monitoring Group. Prior to this, he served as a Supervisor Research Statistics and Policy Analysis in the Research and Planning Division of the Uganda Revenue Authority. Can be reached via: ssuunaster@gmail.com Hon: Dr Abullah H Makame, Member of East Africa Legislative Assembly (EALA): Dr Makame, is a distinguished member of the East African Legislative Assembly (EALA) based in Arusha, Tanzania, where he is a commissioner and a former Chairperson of the Standing Committee in Agriculture, Environment, Tourism and Natural Resources. Dr Makame has served in various senior capacities in both the Government of United Republic of Tanzania and Zanzibar; academically, his docorate is from Birmingham UK and MSc from Strathclyde – Scotland, he holds a Professional Certificate in International Trade from Adelaide and has published both locally and internationally. Dr Makame serves in various boards across the EAC region. Can be reached via email: abdullah.makame@gmail.com

Hon: Dr Abullah H Makame, Member of East Africa Legislative Assembly (EALA): Dr Makame, is a distinguished member of the East African Legislative Assembly (EALA) based in Arusha, Tanzania, where he is a commissioner and a former Chairperson of the Standing Committee in Agriculture, Environment, Tourism and Natural Resources. Dr Makame has served in various senior capacities in both the Government of United Republic of Tanzania and Zanzibar; academically, his docorate is from Birmingham UK and MSc from Strathclyde – Scotland, he holds a Professional Certificate in International Trade from Adelaide and has published both locally and internationally. Dr Makame serves in various boards across the EAC region. Can be reached via email: abdullah.makame@gmail.com Mr Moses Kulaba, Executive Director & Convenor, Governance and Economic Policy Centre: Mr Moses is a political economist, tax and economic diplomat with more than 20 years of active service in international public, private and civil society sector. Prior to joining GEPC he served as the East Africa Regional Manager for the Natural Resources Governance Institute, where he worked with various stakeholders including governments to advance fiscal policies and governance of the extractive sector. Has served on the international board of the EITI and in consultancy roles for UN, DFID and the EU. Can be reached via : moses@gepc.or.tz or mkulaba2000@gmail.com

Mr Moses Kulaba, Executive Director & Convenor, Governance and Economic Policy Centre: Mr Moses is a political economist, tax and economic diplomat with more than 20 years of active service in international public, private and civil society sector. Prior to joining GEPC he served as the East Africa Regional Manager for the Natural Resources Governance Institute, where he worked with various stakeholders including governments to advance fiscal policies and governance of the extractive sector. Has served on the international board of the EITI and in consultancy roles for UN, DFID and the EU. Can be reached via : moses@gepc.or.tz or mkulaba2000@gmail.com

Firstly, the rising temperatures and extended droughts have resulted in a loss of vegetation and negatively impacted gathering and hunting activities undertaken by the Hadzabe people. Their hunting and eating habits have changed as they now have to turn to unconventional hunting methods and eating of endangered animal such as monkeys, baboons and rare bird species to compensate for the dwindling plant and animal species that previously provided food. Increasingly the Hadzabe are gradually becoming a danger to the animals and an ecosystem that they protected for many generations earlier.

Firstly, the rising temperatures and extended droughts have resulted in a loss of vegetation and negatively impacted gathering and hunting activities undertaken by the Hadzabe people. Their hunting and eating habits have changed as they now have to turn to unconventional hunting methods and eating of endangered animal such as monkeys, baboons and rare bird species to compensate for the dwindling plant and animal species that previously provided food. Increasingly the Hadzabe are gradually becoming a danger to the animals and an ecosystem that they protected for many generations earlier. The level of alcoholism and substance abuse has increased as they look for alternative ways to survive the harsh living conditions in a changing natural environment. The leading causes of death are malaria, respiratory diseases, anemia and cardio-circulatory disease and maternal mortality rates amongst the women and children.

The level of alcoholism and substance abuse has increased as they look for alternative ways to survive the harsh living conditions in a changing natural environment. The leading causes of death are malaria, respiratory diseases, anemia and cardio-circulatory disease and maternal mortality rates amongst the women and children.