East Africa’s 2026/27 Budget plans and implications of US-Iran war on energy and economic outlook

Author: Moses Kulaba, Governance and Economic Policy Centre

In February the major East Africa Communities Countries (Uganda, Kenya, Tanzania, Rwanda and Burundi) presented to their budget expenditure framework papers and plans in which governments outlined their tax budget proposals and priorities for 2026/27 financial years. The plans are now tabled before their country’s respective parliamentary committees for scrutiny and deliberation.

This paper reflects on the East African Community (EAC) countries budget and tax proposals in the context of economic and tax justice, equity and fairness and the implications of the US, Israel and Iran war on East Africa’s economic outlook for 2026/27. The paper finds that economic benefits from increased budgetary expenditures have been uneven and the US, Israel and Iran war has adverse implications on the region’s economic performance

According to the framework papers, Kenya plans to spend Ksh 4.7 Trln, Uganda UGx78.24 Trln (U$ 21.78 bln) which is about 12.7% increase and Tanzania will spend a record Tsh61.9Trln representing 9.7 % increase compared to previous budget. The governments will raise from tax and non-tax measures with Tanzania focusing more on domestic tax mobilization strategies due to donor aid restraints arising after the violent 2025 general elections. The countries have laid out key expenditure priorities with Education, security, health, infrastructure ranging among the top.

|

Country |

2025/26 budget |

2026/27 plans |

+/- |

Key Priority areas |

|

Uganda |

UGX 72.4 Tln ($20 B) |

UGX 78.24 Tln ($21.78 B) |

+12.7% |

Econ transformation, Infrastructure, Fiscal Strategy, Infrastructure (EACOP) |

|

Kenya |

Ksh 4.2 T to 4.3 T ( $32-33 Bln) |

Ks4.7Tln |

+173bln |

Education, Security, Health and Agriculture |

|

Tanzania |

Tsh56.49 Trln ($21.7–$22.07 Bln) |

Tsh 61.9 Trln |

+9.7% |

Energy, Health, Education, Domestic Revenue Mobilization |

|

Rwanda |

Rwf 6,952.1 Bln

(US$57.5 Mln) |

– |

– 27.8% (GDP) |

Infrastructure (Bugesera Intl Airport, Recurrent expenditure cuts |

|

Burundi |

Bf 5.2 trln ( $1.77 billion). |

– |

– |

Infrastructure, Agriculture, Social development projects |

|

South Sudan |

SSP 7.00 Trln |

– |

– |

Wages, debt servicing, and infrastructure development. |

|

Dem Republic Congo |

Cf 49,846.8 bln ($17.5 bln to $17.6 bln) |

– |

– |

Security, infrastructure, agriculture, and social services |

Despite the grandeur of the plans, experiences from the past budgets and analysis of their implementation outcome and economic impacts on ordinary citizens shows that the devil lies in the details. Increasingly, the budgets and their tax plans have been not equitable, just and fair.

Over the last three years, the EAC Countries have increased budgetary expenditures, increased taxes and suppressed inflationary pressures but recorded unevenly distributed economic prosperity. Unemployment, income and food poverty are still persistent.

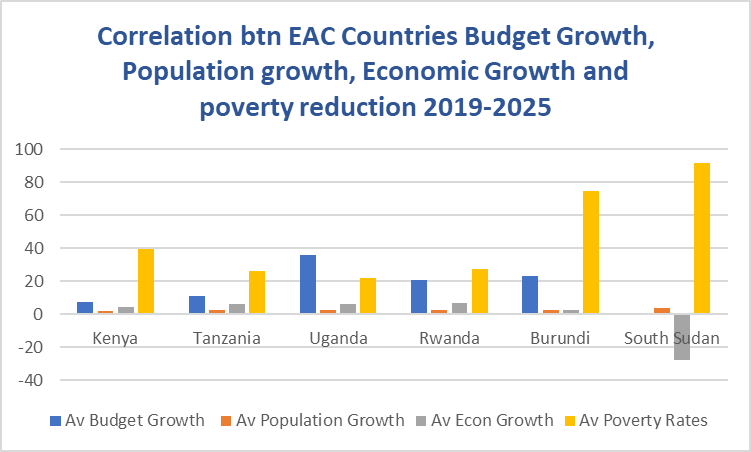

The World Bank reports poverty rates in East Africa are generally high, with significant variations by country and region. In 2022, approximately 39.8% of Kenya’s population lived below the national poverty line. Other estimates for 2022 indicate international poverty rates (at a day) of 42.3% for both Uganda and Rwanda, and 32.4% for Sudan, with rates often higher in rural, arid, and semi-arid areas. Data indicates that while some countries have made progress, substantial challenges remain, with high debt servicing and vulnerability to external shocks affecting poverty reduction efforts

For instance, according to a study by Kenya’s National Bureau of Statistics household food poverty rates have increased and about 65% families in Nairobi barely afford two meals a day over lack of money. As of 2024, approximately 70% of households in Nairobi experienced food insecurity, ranging from moderate to severe. The conditions are worsening with recent reports in 2025 indicated that the majority of residents can no longer afford three meals a day, and many are skipping meals or stopping cooking altogether due to high costs together[i] The situation is worse in the informal settlements where over 65% of Nairobi residents live (The Standard times)

Further reports indicate widening income inequality and impacts in Kenya. While around 25% of Nairobi households fall into the middle-income group, only a small minority (about 3.54% or 58,818 households) belong to the upper-income group, suggesting that for a large portion of the population, purchasing two proper meals daily is a financial challenges

The poverty rates in Tanzania and Uganda remain high and have remained stagnated or declined at very modest rates over the last five years.

Tanzania’s poverty rate remains high, with approximately 49% of the population living below the international extreme poverty line of $1.90 per day, a figure that remained stagnant between 2011/12 and 2018. While economic growth has been steady, about 27% of the population still lives below the national basic need’s poverty line. Poverty is heavily concentrated in rural areas, where over 57% of inhabitants are considered multidimensionally poor[i]

Uganda’s national poverty rate has shown improvement, declining to 16.1% in 2023/24 from 20.3% in 2019/20, according to the Uganda Bureau of Statistics. Despite this, a significant portion of the population remains vulnerable, with 57.2% experiencing multidimensional poverty based on 2016-2022 data. Rural areas, where poverty is concentrated, have seen slight improvements, with poor individuals decreasing to 5.3 million in 2023-2024

Graph showing Budget Expenditure growth, population, economic growth and Poverty reduction trends

Figure 1: GEPC Research Data analysis

Despite what looks like well-structured priority sectors, the expanded budgetary expenditures are yet to be reflected in the pockets of ordinary citizens.

What is ideal budget and economic growth rates to cut poverty

Based on the World Bank and Africa Development bank projections, the national budget are ‘modest’ and insufficient to cut poverty. To put a dent in the poverty rates at the current population growth rates, the economic growth would need to be sustained between 7-10% for a period of about 5 years. To achieve that level of sustained growth the budget expansion rates would require to consistently remain between 15-30%. The governments would require to target high fiscal multiplier efficiency.

With the current budget proposals, projected revenue collections and expenditure priorities characterized by significant portions of the national budgets spent on recurrent expenditure (salaries) and debt serving, achieving poverty reduction and economic justice targets in the EAC countries are unattainable.

Limitations to achieve ideal budget expansions and equitable economic growth for poverty reduction

Moreover, EAC countries’ economies and tax plans are still exposed to large external debts and vulnerable to internal and external shocks. In 2023 Kenya and Uganda experienced violent tax protests. The DRC, Rwanda, Burundi and South Sudan are still affected by conflicts that have stagnated their economic progress.

Rwanda plans to on fiscal consolidation with a reduction from 28.7% of GDP in 2025/26 to 27.8% of GDP in 2026/27 and projected economic growth of approximately 7.1% to 7.5% in 2026, driven by strong performance in services, industry, and continued public investment. However, these plans and growth trajectories are negatively affected by an ongoing conflict in the Eastern DRC which has adverse effects on Rwanda mining and tourism sector.

The DRC and South Sudan struggled to pass their last budgets on time while Burundi has struggled to service a huge external debt burden. The country heavily relies on domestic revenue (including occasion tax hikes on imports and services) and borrowing from domestic banks due to fiscal constraints and lack of external support. The Burundi, DRC and South Sudan experience demonstrate the tragedy of conflict, economic exclusion and meeting public economic expectations in time of crisis.

The high poverty rates, persistent conflicts and failure or delayed passing of the national budgets in our conceptualization constitutes a breach in public expectations, exacerbates the distance between the state and the public, creates further civil apathy and failure to deliver economic outcomes, which can lead to a vicious cycle of poverty economic exclusion, more conflicts and eventual state collapse.

Implications of US, Israel and Iran war on budget and regional economic outlook

The ongoing US, Isreal and Iran war characterized with a spike in oil and gas prices and logistics supply chain disruptions in its first days, will affect energy outlook, may thwart economic growth projections and budget plans in the short and midterm. The impacts will be worse if the war continues for more than six months.

Photo credit: Los Angles Times

The EAC and Middle East economic nexus

The EAC economy has been increasingly integrated with the Middle East, particularly, the Gulf Cooperation Council (GCC) like the UAE and Saudi Arabia through a combination of high-volume trade, strategic infrastructure and financial aid. Since 2015 the Middle East has become to the top logistical hub and EAC’s export partners and The EAC is energy import reliant on the Middle East for petroleum products and Uganda and Kenya have signed fuel agreements to manage supply for potential disruptions. The GCC countries provide aid, infrastructure investment and currency stabilization facilities as was the case with the Kenya-UAE loan in 2025.

EAC countries have struck strategic partnerships beyond commerce. Gulf capital is present in infrastructure investments such as modernization of ports roads and sovereign investments focusing of mining, agriculture, forestry and tourism. This has increased aid dependence and debt exposure to gulf financing. Moreover, the over reliance on Gulf petroleum imports leaves EAC countries’ economies industrial production and transport sectors locked to the gulf and vulnerable to any shocks from the region.

Various models indicate there is a positive correlation of GDP elasticity with respect to world oil prices (i.e the ratio between percentage change in GDP and percentage change in World oil prices). Prolonged high oil prices test global resilience, raising risks for growth, inflation and monetary policy. A 10% increase in oil prices, if sustained for most of the year, is estimated to reduce global economic output by approximately 0.2% and increase global inflation by about 0.4%. This acts as a tax on consumers and increases business production costs, slowing down growth in oil-importing economies.

An increase of 25% would lead to 0.5% loss in GDP and an increase by 50% will lead to 1% of loss of GDP. A doubling of oil prices can cause up to 14% of loss of economic outputs in countries over the years. In less developed countries like those in the EAC, where agriculture sector is the key contributor to GDP and the sector Is relatively less oil intensive due to less developed countries. However, the percentage of GDP loses in these countries are still higher compared to those of developed countries.

Based on these projections, we can the following risks and implications.

Key risks and implications

- Higher energy costs and disrupted logistics and generalized economic confidence shocks that will constitute meaningful drag on economic growth projects to slow down in Q4 of the 2025/26 budgets and Q1 and Q2 of the 2026/27 budgets and generally a gloomy economic outlook if the war continues for more than six months.

- Middle East export and import market disruptions affecting largely EAC’s agriculture sector, which is the major economic growth driver. The war has affected exports from the middle east of Ammonia and Sulphur, which are vital ingredients for the production of fertilizers, a vital product supporting the agricultural sector.

- Potential decline in aid, infrastructure investments and budget support from the Middle East as the GCC look inwards to finance their defence and war efforts. This will also trigger an aid squeeze from other regional blocks such as the EU as they focus on protecting Europe.

- Geopolitical pressures for realignment as the major contending powers the US and Isreal pressure EAC countries to choose sides, given some of their historical strategic and cultural relationships with Iran as a source of energy.

- The war represents in my theoretical construction a parody of the ‘Economic Big Boss and the Babies’, in international relations where the larger economic powers dictate the terms and the ‘babies’ deal with the negative consequences irrespective of their will, choice, location and contribution. In this construction of international relations one dominant state or group of states acting in consent and consort and through various means including state craft create an asymmetrical power relation with others analogous to a ‘Parent and baby relationship, where the stronger power exerts its spere of dominance beyond the physical and juristic territorial boundaries as recognized under international law, compelling the weaker states to act and respond to demands, desires, actions and geopolitical effects of the bigger state.

- The world is yet to fully recover from the loss of markets and inflationary pressures the US global tariffs and were working towards realignment of new trading partners in the middle east. This war will add uncertainty to this economic quagmire. As the global economy snarls and slags, the EAC economies could follow too, albeit with levels and pace.

- The success of the US and its allies in the middle could increase appetite for it to attack elsewhere setting in motion a spiral of violence, war and economic disruptions around the world. It is widely believed that the US’s success in Venezuela and Isreal’s success in Palestine and Lebanon could have motivated its attack of Iran.

Key recommendations

Tax and budgetary actions.

Reclaim public trust and social contracts to serve via a just, fair and equitable taxes and redistributive budgetary policies.

To mitigate the unequitable distributed economic growth and achieve East Africa’s budget trajectory and economic outlook will require something beyond the traditional ‘invisible hand’ economic theory approach to correct. The traditional approach suggests free markets naturally achieve optimal efficiency.

Keynesian economics fundamentally challenges the traditional “invisible hand” concept, arguing instead that economies can get stuck in prolonged recessions. Keynes believed the “hand” is not self-regulating during crises, necessitating active government intervention (fiscal policy and other interventions) to manage booms and busts or serious economic disruption.

Strategic recommendations

- Pursue intra Africa regional trade so as to shelter against external shocks in the middle east

- Increase investment in renewable energy sources to reduce over reliance from Middle East fossil petroleum

- Pursue new geopolitical realignments to hedge against the potential fall out and of the middle east and other turbulent blocks

[i] World Bank Group: Poverty and Equity brief, Sub-Saharan Africa, Tanzania April, 2020 available at : https://databankfiles.worldbank.org/public/ddpext_download/poverty/33EF03BB-9722-4AE2-ABC7-AA2972D68AFE/Global_POVEQ_TZA.pdf#:~:text=Using%20the%20international%20extreme%20poverty%20rate%20of,people%20are%20considered%20poor%20along%20this%20line.

[i] The Standard Newspaper; Why majority of Nairobi residents can no longer afford to eat, February, 08, 2025, available, at https://www.standardmedia.co.ke/national/article/2001511317/why-majority-of-nairobi-residents-can-no-longer-afford-to-eat

[ii] Apolo Rosabella, Strengthening food and nutrition security in Nairobi’s informal settlements, Africa Cities Research Consortium (ARC), February, 2024 available: https://www.african-cities.org/new-paper-strengthening-food-and-nutrition-security-in-nairobis-informal-settlements/#:~:text=New%20paper:%20Strengthening%20food%20and%20nutrition%20security%20in%20Nairobi’s%20informal%20settlements,-Feb%208%2C%202024&text=Since%20independence%2C%20Kenya%20has%20grappled,residents%20of%20low%2Dincome%20households.

The East African Oil Pipeline project received significant boots in April 2021 with Uganda with a series of key oil infrastructure related agreements signed between the government of Uganda and Tanzania and the oil companies for the East Africa Crude Oil Pipeline (EACOP) project to transport crude from Uganda to the Tanzania port of Tanga.

The East African Oil Pipeline project received significant boots in April 2021 with Uganda with a series of key oil infrastructure related agreements signed between the government of Uganda and Tanzania and the oil companies for the East Africa Crude Oil Pipeline (EACOP) project to transport crude from Uganda to the Tanzania port of Tanga.

The total receipts from services recorded a positive trend due to also the increase in the transport sector, which rose from $1.14 billion in 2017 to $1.22 billion in 2018. MER reported that following an increase in travel and transport foreign receipts, the total foreign exchange receipt from services was $4.01 billion in the year to December 2018, an increase of $182.8 million from the amount registered in the corresponding period in 2017

The total receipts from services recorded a positive trend due to also the increase in the transport sector, which rose from $1.14 billion in 2017 to $1.22 billion in 2018. MER reported that following an increase in travel and transport foreign receipts, the total foreign exchange receipt from services was $4.01 billion in the year to December 2018, an increase of $182.8 million from the amount registered in the corresponding period in 2017